Tax planning is no longer a “nice-to-have” conversation for Canadian Financial Advisors — it’s central to delivering real value.

Clients don’t just want investment returns. They want to know:

- Are we minimizing taxes?

- Are we structuring this correctly?

- Are we leaving money on the table?

The Canadian tax system creates both complexity and opportunity. Advisors who can model strategies clearly and compare outcomes visually are in a powerful position to differentiate themselves.

Here’s how you can use Snap Projections to optimize tax planning for three common (and high-impact) client scenarios.

How to help a 35-year-old client save for a first home: TFSA or FHSA?

The introduction of the First Home Savings Account (FHSA) created a significant tax planning opportunity — and confusion.

Clients ask:

- Should I use my TFSA instead?

- Can I use both?

- What happens if I don’t buy a home?

- Which gives me the biggest advantage?

For a 35-year-old professional planning to buy within 3–7 years, this decision can materially impact:

- Current tax savings

- Long-term compounding

- Retirement assets

- Flexibility

If you’re not modelling it, you’re guessing.

The Tax Planning Considerations

FHSA advantages:

- Contributions are tax-deductible (like an RRSP)

- Withdrawals for a qualifying home purchase are tax-free (like a TFSA)

- Growth is tax-free

TFSA advantages:

- Contributions are not deductible

- Withdrawals are tax-free for any purpose

- No requirement to purchase a home

But the optimal answer depends on:

- Marginal tax bracket

- Expected timeline to purchase

- Cash flow

- Other registered room availability

- Backup plan if no home is purchased

How Snap Helps

With Snap Projections, you can:

- Model annual FHSA contributions and tax refunds

- Compare contributing to a TFSA instead

- Show projected net worth differences at purchase date

- Show retirement impact if funds remain invested long-term

For example, you can create two scenarios:

Scenario A: $8,000/year into FHSA

Scenario B: $8,000/year into TFSA

Snap will illustrate:

- Immediate tax savings from FHSA contributions

- Account growth over time

- Long-term retirement value if unused

- Impact on future RRSP room if rolled over

This moves the conversation from theory to evidence.

Instead of saying “FHSA is usually better,” you show the math — including the long-term opportunity cost.

That’s strategic tax planning.

How to help a 58-year-old couple review their decumulation plan and increase after-tax retirement income

Decumulation is where tax planning can become next level valuable.

At age 58, a couple is often:

- 2–7 years from retirement

- Holding large RRSPs

- Unsure about CPP timing

- Concerned about taxes in their 70s

- Worried about running out of money

Without a tax-efficient drawdown strategy, clients can:

- Pay unnecessary taxes

- Trigger OAS clawbacks

- Leave less to beneficiaries

- Create avoidable volatility in retirement income

This is where you move from portfolio manager to strategic planner.

The Key Tax Planning Questions

- Should we start drawing RRSPs before 65?

- Should we smooth income over time?

- Should we target a specific tax bracket?

- When should we start CPP and OAS?

- Should we convert some RRSP assets early?

In Canada, government benefits like the Canada Pension Plan and Old Age Security interact heavily with taxable income.

Poor sequencing can increase lifetime tax payable significantly.

How Snap Helps

Snap allows you to build multiple decumulation strategies and compare:

- Total lifetime tax paid

- Annual after-tax retirement income

- Government benefit impacts

- Estate value

You can create scenarios such as:

Scenario A:

- Defer RRSP withdrawals until mandatory RRIF conversion

- Take CPP at 65

Scenario B:

- Start drawing RRSPs at 60

- Defer CPP to 70

- Target a consistent taxable income level annually

Scenario C:

- Blend TFSA withdrawals strategically to manage taxable income

Snap visually demonstrates:

- Income consistency over time

- Tax spikes

- OAS clawback exposure

- Net after-tax income

Often, modest early RRSP withdrawals to “fill up” a lower tax bracket can significantly increase after-tax lifetime income.

When clients see that:

- Total lifetime tax drops

- Retirement income becomes smoother

- Estate values improve

They recognize the value of proactive planning.

This isn’t about returns. It’s about structure.

How to build multiple scenarios to compare estate outcomes at different ages using Taxable Income Targeting

Estate planning conversations are often emotional — but should be tax-driven.

In Canada, there is no estate tax — but there is deemed disposition at death. Large RRSP or RRIF balances can create substantial tax liabilities.

Clients who assume their estate will receive the full value of their registered accounts are often wrong, so early planning and discussions are essential.

Strategic taxable income targeting can dramatically change estate outcomes in some cases.

What Is Taxable Income Targeting?

Taxable income targeting is the strategy of:

- Intentionally withdrawing funds

- Managing income levels

- Staying within specific tax brackets

- Avoiding clawbacks

- Reducing large final tax bills

Instead of deferring all taxes as long as possible, you manage them over time.

How Snap Helps

With Snap, you can:

- Set annual income targets

- Adjust withdrawal sequencing

- Compare tax paid at death

- Model estate values at various life expectancies

You can build multiple scenarios:

Scenario A: Maximum tax deferral

- No early RRSP withdrawals

- Large RRIF balance at death

Scenario B: Moderate income targeting

- Draw down RRSPs gradually between 60–72

- Maintain consistent marginal tax rate

Scenario C: Aggressive income smoothing

- Accelerated withdrawals in lower-income years

- Larger TFSA balances preserved

Snap will illustrate:

- Total lifetime tax paid

- Tax payable at death

- After-tax estate value

- Net benefit to beneficiaries

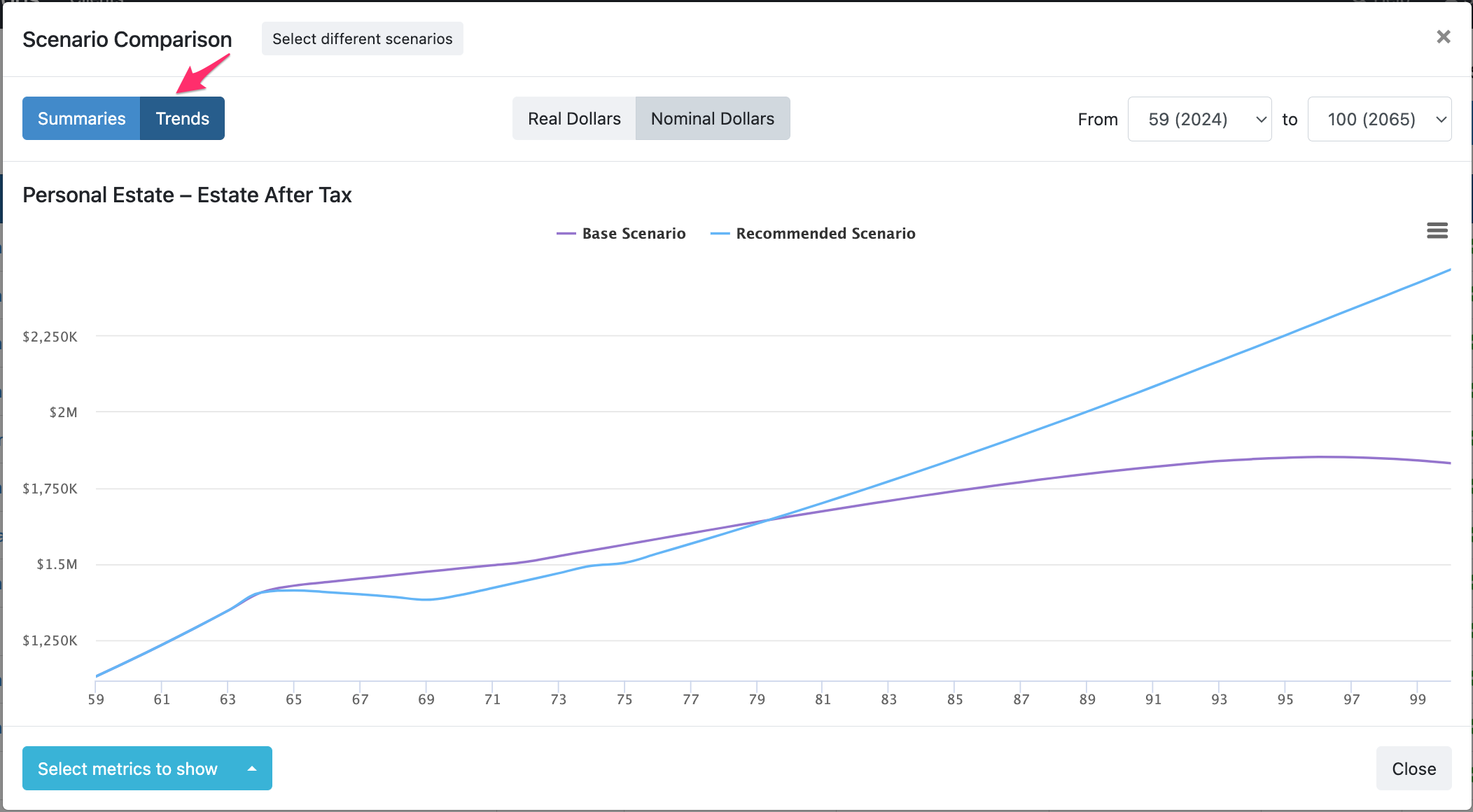

When clients see the estate value at age 85, 90, and 95 under each strategy, the impact becomes tangible.

This is an example of two scenarios being compared to understand the net difference in Estate After Taxes. If the clients lives past age 79, the Recommended Scenario becomes the optimal choice.

Often, strategic income targeting:

- Reduces the tax bill at death

- Increases after-tax inheritance

- Provides more retirement flexibility

This creates a powerful advisory moment.

You’re no longer just projecting growth — you’re optimizing outcomes.

Watch the tax planning tutorial and see it all in practice

On March 3rd, 2026, 140 Canadian Financial Advisors and Planners attended this CE-accredited tax planning webinar and learned exactly how to execute the strategies mentioned above. Watch the replay now! Live attendance was required for CE Credit.

The easiest way to switch from one planning software to another

If moving your client files and plans is keeping you in the wrong financial planning software, check this out. Snap has recently released a brand new ai-driven data assist feature that completely eliminates manual data entry when you have existing plans or even client documentations you can upload. If you’re curious, you can learn about how the ai data-assist feature works.

Start a 14-day Free Trial of Snap Projections

Canadian Financial Advisors, Planners, and Investment Managers are eligible to start a 14-day Free Trial of Snap Projections financial planning software.

The bigger opportunity: Differentiating yourself as a Tax Planning Strategist

Canadian Financial Advisors who lead with tax strategy differentiate themselves in meaningful ways.

When you can:

- Compare FHSA vs. TFSA with real projections

- Optimize decumulation for higher after-tax income

- Demonstrate estate value differences under multiple tax strategies

You move from product conversations to strategic planning conversations.

Snap Projections enables you to:

- Build scenarios quickly

- Compare outcomes visually

- Quantify tax savings

- Deliver one-page summaries clients understand

Tax planning isn’t just about minimizing this year’s tax bill.

It’s about:

- Lifetime tax efficiency

- Income sustainability

- Government benefit optimization

- Estate maximization

When clients see the numbers clearly — when they understand how different strategies affect their retirement income and their legacy — your value becomes obvious.

In a competitive advisory environment, the ability to model tax optimization in real time is more than a feature.

It’s a growth strategy for your practice.

Because when you can confidently say, “Let’s compare that,” you’re not just giving advice — you’re proving it.