Effectively managing contributions and withdrawals to maintain a specific taxable income and marginal tax rate can have a profound impact on reducing your clients’ overall tax burden—both in the short term and over the course of their retirement.

With Snap’s new functionality, you can now set a customized annual Taxable Income Target for each year in your projections. Snap will then automatically adjust cash flows—strategically determining when to draw from registered, non-registered, or tax-free accounts—to keep income as close to that target as possible. This automation not only saves Financial Planners time on manual adjustments but also ensures tax efficiency is consistently optimized year after year.

By smoothing income and avoiding unnecessary jumps into higher tax brackets, you can help clients preserve more of their wealth, extend the longevity of their portfolios, and create a more predictable, stable retirement income stream—all while demonstrating clear, quantifiable value in your advice.

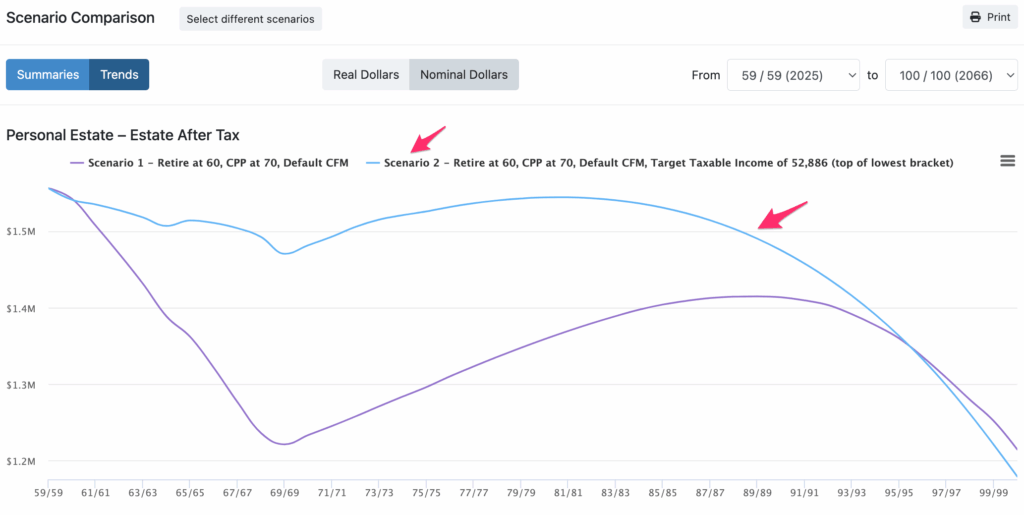

You can use the existing Comparing Scenarios tool to analyze how different Taxable Income strategies affect your client’s outcomes. Scenario 1 uses the default Cash Flow Management (CFM) Order for withdrawals of non-registered, TFSA, and registered accounts. Scenario 2 uses the same CFM Order and withdraws extra registered money to help the client reach the top of the lowest tax bracket in Ontario. The Taxable Income Targeting approach increases the projected Estate After Tax in almost all future years. At the largest difference, there’s a $250K advantage for the second scenario using the Target.

Why we created Taxable Income Targeting

As always—they asked so we built it.

Advisors have always used Snap to build and illustrate customized retirement drawdown strategies. As tax planning becomes an even greater focus during client meetings, many of Snap’s Advisors have requested a faster, more intuitive way to manage taxable income—particularly when illustrating strategies like RRSP drawdowns before age 71, minimizing OAS clawback, or smoothing marginal tax brackets.

This is why we created Taxable Income Targeting. This feature allows Advisors to define a target for taxable income in specific years, with Snap then doing the heavy lifting to automatically and transparently manage withdrawals from RRSPs, RRIFs, and other accounts accordingly—reducing reliance on manual overrides.

This feature makes it easier for Advisors to communicate tax strategies, support more efficient planning conversations, and demonstrate the value of their withdrawal planning recommendations.

What Advisors said about the need for Taxable Income Targeting

Clients are increasingly aware of the need to understand and plan for potential tax implications throughout their retirement.

For Advisors, this means that in addition to building optimized drawdown plans, they also need to explain and communicate the strategies in a way that builds trust and understanding.

For example, let’s say an Advisor runs a base scenario and applies a taxable income cap—for example, to avoid OAS clawback.

Snap will then:

- Automatically draw from Registered accounts up to the cap

- Use other sources (TFSA, Non-Registered) to meet remaining income needs

- Reinvest any surplus income if spending is lower than the target, based on the client’s pre-determined default withdrawal order

Advisors can quickly see what’s happening in the plan, follow the logic, and walk their clients through the strategy—all in real time.

Taxable Income Targeting improves transparency and helps Advisors illustrate the tax advantages of thoughtful drawdown strategies, all while simultaneously reducing planning time and manual work.

How Advisors tell us they plan to use this new Taxable Income Targeting functionality

- Cap taxable income to avoid OAS clawback or stay within lower marginal tax brackets

- Level out marginal tax brackets across multiple years

- Compare early vs. deferred RRSP/RRIF withdrawals

- Maximize lower tax brackets in early retirement

- Automatically reallocate surplus income into tax-efficient savings strategies

- Follow, control and explain decumulation strategies quickly during client meetings

What Advisors say about how this new feature stacks up against other financial planning software

- Easier to understand what the software is doing—and why

- More transparent, with less time spent analyzing unexpected results

- Better integrated into the planning flow—not a separate tool or calculator

- Enables real-time discussion and strategy testing, not just backend modelling

- Designed to support what advisors already do in practice, now with speed and clarity

Next steps

Canadian Financial Advisors, Planners, and Investment Managers are eligible to start a 14-day Free Trial of Snap Projections financial planning software.