If you’re a Financial Advisor and want to increase your client retention, check out our hub featuring expert insights, proven strategies, and industry best practices.

Get the Financial Planner's Toolkit

CRM3: Value is no longer shown by the return of your portfolio

The Canadian wealth industry is entering a new phase—one where transparency is no longer partial, and where performance alone is no longer enough to justify advice. Kaitlyn Lawson, head of practice management with CI Global Asset Management, was quoted in an article...

Double Your Time. Discover More Value. Snap Projections Is Offering a 30-Day Free Trial This August.

Snap's semi-annual promo is here Choosing the right financial planning software is an important decision. It isn't just about comparing features, it’s about finding a solution that fits naturally into your advice process, helps you deliver better client outcomes, and...

Income splitting in Canada: how it works, benefits, and implementation

Your client asks about income splitting during their retirement review. Suddenly, you are sorting through Tax on Split Income (TOSI) rules, attribution traps, and Canada Pension Plan (CPP) sharing. This resource will help you categorize client questions quickly,...

Permanent life insurance: types, benefits, and top policies

Permanent life insurance provides lifelong coverage with cash value growth. But moving from "what is it?" to "does it fit?" takes a clear breakdown, realistic cost anchors, and a walkthrough of what happens when clients tap cash value. This article will help you...

Why Financial Advisors Still Need Financial Planning Software in the Age of ChatGPT

Recent headlines have highlighted just how important it is for professionals to verify AI-generated information. In one widely reported Canadian case, legal professionals faced scrutiny after artificial intelligence generated court citations that simply did not...

Total Cost Reporting: What Advisors Need to Do Before 2027

The next major evolution in Canadian investment regulation is coming—and it will change how clients see cost, value, and advice. With the transition from CRM2 to CRM3 (also known as Total Cost Reporting, or TCR), Canadian Financial Advisors, Planners, and Investment...

Tech Rules for CFPs & QAFPs | FP Canada Standards Council

Did you know that there are new technology rules for Financial Planners? This blog post was originally published on October 28, 2021, and was last updated on June 17, 2026. In July 2021, the FP Canada Standards Council added two new rules to their Standards of...

AI-driven Financial Planning: Automate tasks & keep Advisors in control

Artificial intelligence seems to be everywhere right now. Every week, a new platform claims it can automate workflows, generate advice, replace manual processes, or completely transform the way Financial Advisors work. While there is certainly excitement around the...

Why the financial planning process is the most scalable growth strategy for Financial Advisors

For years, many Financial Advisory relationships have revolved around investment performance. But in today’s environment, especially with increasing fee transparency through Total Cost Reporting, clients are evaluating Advisors differently. They’re asking: What value...

Why Total Cost Reporting Is an Opportunity for Financial Advisors to Scale

For many Canadian Financial Advisors, the upcoming shift to CRM3—also known as Total Cost Reporting (TCR)—initially feels like a compliance burden. More disclosure. More scrutiny. More client questions. But that framing misses the bigger picture. CRM3 is not just a...

Term life insurance Canada: needs analysis steps for Advisors

Term life insurance Canada questions come up all the time. Even so, many recommendations still lean on outdated rules of thumb and quick "napkin math" that do not reflect a client's actual liabilities, timelines, and offsets. That is when coverage shifts mid-meeting...

New feature release: Automated Financial Recommendations

We are thrilled to announce that another much-anticipated feature is now live in Snap Projections. Financial Recommendations was created to automate the process of testing different optimization strategies in order to identify strong, practical and implementable...

CRM2 versus CRM3: What’s the Difference for Financial Advisors?

For Canadian Financial Advisors, regulation has steadily moved in one direction over the past decade: greater transparency. From the rollout of CRM2 to the upcoming implementation of CRM3, or Total Cost Reporting, the message from regulators is clear. Clients should...

How to calculate ACB: formula, table, and adjustments

Accurate capital gains reporting depends on adjusted cost base (ACB). But ACB tracking can break down when clients have reinvested distributions or return of capital. Broker statements often miss those adjustments, so you end up rebuilding ACB from slips, fund...

How Canadian Financial Advisors can save hours this tax season with ai data assist

Advisors can turn tax season into an opportunity with ai-powered data assist Tax season has always been a paradox for Financial Advisors. On one hand, it’s one of the most valuable times of year to deliver planning insights and deepen client relationships. On the...

After tax cash flow (ATCF): How to calculate, impact, & examples

Gross income does not tell the full story, especially when you are planning for retirement, big purchases, or long‑term cash flow needs. What really matters is how much money clients actually keep after taxes, deductions, and benefits are figured in. Understanding...

Managing a FHSA (First Home Savings Account): The guide

Buying a first home can feel out of reach, especially with rising prices and the need for a large down payment. But with the right plan, your clients can save faster while reducing their overall tax burden. Many Canadians don't yet realize how much the new First Home...

TFSA contribution limit: How to maximize clients’ savings

Many clients miss out on thousands in tax-free savings because they don't fully understand how the TFSA contribution limit works. Even small mistakes, such as re‑contributing too early or guessing contribution room, can lead to penalties or lost growth. As a Financial...

Financial Planning is hard enough—stop fighting with your software!

In today’s advice landscape, Canadian Financial Advisors are expected to deliver more than product recommendations. Clients want clarity. They want certainty. They want to understand how today’s decisions impact the rest of their lives. That’s where clear, fast, and...

Deliver more value this year with tax planning optimizations

Tax planning is no longer a “nice-to-have” conversation for Canadian Financial Advisors — it’s central to delivering real value. Clients don’t just want investment returns. They want to know: Are we minimizing taxes? Are we structuring this correctly? Are we leaving...

Reclaim Your Planning Hours with Snap Projections’ AI Data Assist

If you’re a Canadian Financial Advisor, you already know where too much of your week goes. Not in strategy. Not in meaningful client conversations. Not in refining recommendations. It goes into data entry. Investment accounts. Registered plans. Insurance policies....

Life insurance needs analysis: How to determine what clients need

Most families never expect financial hardship until it happens. The uncertainty your clients could face if an unexpected loss left them without a safety net can be scary to talk about. However, as the Advisor, you know it will be in your clients’ best interest to have...

Introducing Snap’s ai data-assist: No more manual data entry or errors

Turn client documents into usable plans—fast We are excited to announce that Advisors can now instantly build first drafts of financial plans using client documents with Snap's new data assist feature. Entering data manually is slow and error-prone. API and...

Corporate life insurance: How it works & key tax benefits

Many Canadian business owners don't realize how much risk they carry if a key person suddenly passes away. Losing a founder, owner, or critical team member can strain cash flow, disrupt operations, and create uncertainty, especially when insurance coverage is...

CPP enhancement: Purpose, implementation, and benefits

Retirement security in Canada is changing, and the CPP enhancement is at the centre of this shift. You may have heard about the updates, but knowing what they mean for you and your clients is important. The new CPP rules affect contributions, future income, and how...

RRIF withdrawal rates: What Financial Advisors need to know

RRIF withdrawal rates have a big impact on your clients' retirement income. The minimum amounts rise as clients get older, so Advisors need to understand how these rules work. This overview explains the key RRIF rules in a simple way. You will see how different...

OAS clawback: How it works, implications, & how to minimize risk

Many Canadians do not realize their government retirement benefits can decrease if their income gets too high. The OAS clawback lowers Old Age Security payments once clients pass a certain income level. You may be working with clients who are worried about losing...

Making the most of unused RRSP contributions: A guide for Advisors

Unused RRSP contributions can help clients when used the right way but they can also cause problems when they are not managed properly. Many Canadians do not know that these unused amounts can give them helpful flexibility in future years. Advisors who understand...

What is a defined benefit pension plan? A breakdown for Advisors

A defined benefit pension plan gives steady income in retirement. This type of pension can guide a client's choices for many years. Many Advisors know it is valuable, but the details can still be confusing. This article explains what a defined benefit pension plan is....

Retirement incoming planning optimizations to help your clients

September's retirement income planning webinar is a must-watch if your clients include pre-retirees. When your pre-retiree clients have questions, what is your process to provide answers and options? This lesson includes actionable retirement income planning...

Financial Planning for Younger Couples: Building a Strong Foundation With the Right Tools

Why young couples need a strong financial plan Starting life together as a couple is exciting—but it also comes with major financial decisions. From buying a first home, to raising children, to planning for retirement, the choices couples make early can shape their...

Advisors Can Help Clients Reduce Taxes by Moving Non-Registered Investments Into a TFSA

The problem with non-registered accounts Many Canadians accumulate wealth in non-registered accounts—whether through savings after maxing out RRSPs, inheritances, or simply because they haven’t been strategic about account types. While non-registered accounts are...

Why Advisors Should Conduct Personalized Insurance Needs Analyses

Why insurance planning deserves more attention Life, disability, and critical illness insurance are the foundation of many clients’ financial security. Without proper coverage, even the best-laid retirement or investment plans can be derailed by the unexpected. Yet...

This December Only: Double the Free Trial — Two Full Months of Risk-Free Planning with Snap Projections

December is a unique month in the world of financial planning. While markets slow and client meetings ease up, Advisors finally get one thing they rarely have during the busy year: time. And this year, that time is about to go even further. For December only, Snap...

Help Clients Make Smarter RRSP and TFSA Decisions with Personalized Financial Planning

Why personalization matters in financial planning One of the most common questions clients ask their Financial Planner or Advisor is:“Should I put money in my RRSP or my TFSA?” On the surface, it seems straightforward. Both are tax-advantaged savings accounts designed...

How Financial Planners and Advisors Can Save Time and Reduce Errors in the Planning Process

The challenge of time and accuracy in financial planning Financial Advisors and Planners wear many hats: strategist, coach, educator, and analyst. But two ongoing challenges come up in almost every practice: time and accuracy. Building financial plans can take...

Why Financial Planners Should Compare Multiple Scenarios to Optimize Client Outcomes

Financial planning is never one-size-fits-all. Each client has unique goals, challenges, and preferences. While one strategy may look strong on paper, it might not align with a client’s lifestyle or risk tolerance. That’s why comparing multiple scenarios is so...

Financial planning process: How to build & optimize plans in Snap

Snap Projections is designed to make financial planning faster, clearer, and more collaborative for Advisors and their clients. In this training series, we walked through every core feature—from setting up new clients and entering data, to customizing cash flow,...

How Taxable Income Targeting Helps Clients and Adds Value to the Financial Planning Process

For many clients, taxes are one of the biggest expenses they’ll face throughout life—especially in retirement. While saving and investing strategies are critical, effective tax planning can make just as much of a difference in preserving wealth. Yet many clients don’t...

One-page financial plan: template and checklist for 2026

Today’s clients expect financial advice that’s clear, visual, and actionable. Long reports can overwhelm—what they value most is a simple snapshot that connects their goals to a concrete plan. A one-page financial plan does exactly that. It condenses a client’s...

How Financial Advisors Can Provide Better Recommendations and Options to Clients

Financial planning isn’t just about crunching numbers—it’s about helping clients make confident decisions. Clients come to Advisors with big questions: When can I retire? How much can I spend? Am I saving enough? The most successful Advisors don’t just present data....

What financial planning questions do young couples have?

For young couples, financial planning starts with questions. For Advisors, each question is an opportunity to build trust and show value. By using Snap Projections in discovery meetings, you can move from uncertainty to clarity faster—helping couples see that...

How Financial Advisors and Financial Planners can convert more prospects

This CE-accredited webinar is about having better conversations that will increase client engagement & convert more prospects. This was filmed on Tuesday, July 22nd, 2025, at 1pm ET. Live attendance was required to be eligible for CE Credit. During the 60-minute...

Financial life stages: A guide for Advisors

Clients rarely reach major financial milestones by chance. Each life chapter, starting a career, raising a family, or planning for retirement, brings new priorities and decisions. Yet, many clients may not see these transitions coming, and even fewer may feel...

Provide better tax planning advice and improve your clients’ tax efficiency

This tax-focused financial planning webinar was filmed on June 24, 2025. Live attendance was required to be eligible for CE Credit. Comparing Scenarios for increased tax efficiency As we move into the case study, we’re going to be building out multiple scenarios that...

Trust and estate planning: key financial and legal considerations

Trust and estate planning is a crucial aspect of financial planning for Advisors and their clients, and it can be a very complicated topic. Whether your clients have a high net worth or not, it is important to engage with them while you help them navigate these...

The retirement checklist 101: Key steps to discuss with clients

Guiding clients through the complexities of retirement planning is a core part of your value as a Financial Advisor—a task made even more pressing by surveys that show over 75% of Canadians are worried they won't have enough money in retirement, highlighting the...

Cash flow analysis: how to prepare and explain concepts to clients

Advisors who want to provide clients with a comprehensive understanding of their financial situation must perform a cash flow analysis. This article addresses the importance of cash flow analysis for Financial Advisors and how professionals can effectively prepare...

The role of an Independent Financial Advisor: key responsibilities

Navigating the complexities of personal financial affairs can be challenging for clients, especially when they're just getting started. It's often hard to know where to begin, and there are so many factors to consider. How do they achieve their financial goals when...

Financial Advisor leads: top 14 strategies & tips for growth

Generating the right Financial Advisor leads is more than a numbers game—it's about connecting with people who truly need your expertise, yet a recent Deloitte report found that 78% of Advisors cite lead generation and referrals as their biggest growth hurdle. With...

How finfluencers are influencing client mindsets

You can find a finfluencer for nearly every financial topic, from investing in stocks to maximizing your RRSP to advanced cryptocurrency trading strategies. With just a few taps, Canadians can access financial commentary delivered through bite-sized videos, personal...

Wrap personalized insurance recommendations into your financial planning

This financial planning webinar is all about learning easy-to-execute strategies to help you wrap data-driven, personalized insurance recommendations into your financial planning with complete transparency. Please note: this session was recorded on May 20, 2025 and...

Why Financial Advisors Should Help Clients Maximize TFSA Top-Ups

Why TFSAs matter in financial planning The Tax-Free Savings Account (TFSA) has become one of the most powerful tools available to Canadian investors. With tax-free growth and tax-free withdrawals, it’s an essential vehicle for both short-term flexibility and long-term...

Top 12 Financial tech tools for growth in 2026

The financial landscape is evolving daily thanks to technology and the emergence of savvy investors seeking personalized, tech-driven financial solutions. Recent McKinsey analysis indicates that adoption of generative-AI tools can save Advisors time, underscoring how...

Stress testing in risk management: what you need to know

Uncertainty is one of the biggest challenges in financial planning and business management. Market downturns, inflation spikes, sudden income loss, or unexpected operational disruptions can derail even the most carefully built strategies. For Financial Advisors and...

Decumulation strategies: A guide to retirement income planning

Retirement planning is more than just saving for the future — it’s about strategically using those savings to sustain a fulfilling and financially secure lifestyle. This process, known as decumulation, involves transitioning from building wealth to effectively...

Cash flow projection template: What it is and how to use it

Financial Advisors regularly create financial plans to help clients achieve their goals. To do this effectively, they need to invest time and effort to understand each client’s unique financial situation, including their objectives, risk tolerance, and capacity. Once...

What is scenario analysis? Benefits, types, and examples

Preparing for the future is rarely simple. Uncertainty is a constant, and the most effective strategies are those that embrace flexibility and plan for the unexpected. Scenario analysis provides a robust framework for evaluating possible outcomes, anticipating...

How to get clients as a Financial Advisor: 7 proven ways

Whether you're building your book of business or expanding an established practice, bringing in new clients often presents a meaningful challenge for Financial Advisors. In a landscape that includes robo-advisors, financial influencers, and a constant stream of...

Financial planning steps: The ultimate guide for Advisors

Clients today seek more than generic advice; they are looking for clarity, control, and a plan they can trust. Yet many underestimate the value that comes from a truly personalized financial roadmap. As a Financial Advisor, following a clearly defined planning process...

Goal-based financial planning: A practical Advisor guide

Financial Advisors are often on the lookout for strategies that deepen client relationships, create an environment of trust, and genuinely connect financial actions to a client’s life plans and goals. Goal-based financial planning is a powerful methodology that...

High-net-worth clients: Definition, criteria, and growth strategies

Serving high-net-worth (HNW) clients represents a significant opportunity for Financial Advisors and Wealth Managers. This discerning segment with substantial investable assets and intricate financial lives demands a highly personalized approach to wealth management....

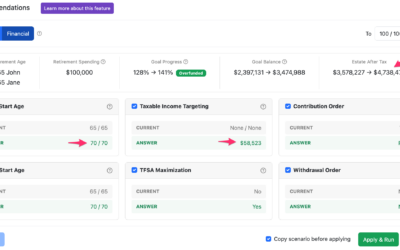

![Automated Taxable Income Targeting [new feature update in Snap]](https://snapprojections.com/wp-content/uploads/2016/07/retirement-income-planning-400x250.webp)

Automated Taxable Income Targeting [new feature update in Snap]

Effectively managing contributions and withdrawals to maintain a specific taxable income and marginal tax rate can have a profound impact on reducing your clients’ overall tax burden—both in the short term and over the course of their retirement. With Snap’s new...

Financial Advisor business plan: A guide to going independent

Starting an independent Financial Advisory practice can be both exciting and challenging. Many Advisors pursue independence to gain more control, build stronger client relationships, and shape a business that reflects their values. Making the move from employment to...

16 Financial Advisor interview questions to hire top talent

The quality of your Financial Advisory team directly impacts your firm's growth, reputation, and ability to deliver exceptional services. An effective hiring process can ensure that your firm is staffed with capable professionals and has a client-centric culture that...

10 client rapport strategies to grow your financial practice

Building long-term relationships with clients is one of the foundations of a successful practice in the financial services sector. Advisors and Planners who focus on building strong client relationships are often in the best position to improve client retention, earn...

Financial advertising: Strategies, trends, and regulations

Attracting the right clients and growing a sustainable practice requires more than technical expertise—it takes clear, consistent communication that reflects your values, process, and professionalism. Today, prospective clients often assess a Financial Advisor’s...

Managing client expectations: A guide for Financial Advisors

Helping clients form realistic and informed expectations is an important part of effective Financial Planning. While investment strategies and portfolio management play a role, much of an Advisor’s value also lies in supporting clients as they navigate financial...

What is holistic financial planning? Key principles explained

Financial planning is evolving and has shifted from product-focused conversations to more personalized, client-centred approaches. Today’s clients are looking for strategies that reflect not just their finances, but also their values, goals, and life experiences. In...

Client onboarding: Steps to build trust for Financial Advisors

The initial interactions a Financial Advisor has with a new client are critical. This period, known as client onboarding, sets the foundation for what will hopefully become a long and mutually beneficial relationship. A well-structured and thoughtful onboarding...

Advisory Team leadership: How to guide and grow your team

Leading an Advisory Team involves more than task delegation—it’s about fostering a collaborative environment where team members can do their best work and deliver meaningful value to clients. As client expectations shift and practices grow, effective leadership plays...

14 essential Financial Advisor skills & how to develop them

As you know, a Financial Advisor’s duties go beyond the number-crunching aspects of their role. To build strong client relationships and deliver long-term value, Advisors often benefit from a mix of technical knowledge and interpersonal strengths. In this article, we...

Best sales training for Financial Advisors: Courses & tips

Financial Advisory is a relationship-driven profession where lasting success often stems from earning trust and communicating value clearly. While the word “sales” may carry traditional associations, in the context of Financial Planning, it’s less about persuasion and...

Creating a Financial Advisor value proposition: 10 effective tips

As a Financial Advisor, Planner, or Investment Manager who wants to differentiate themselves and stand out from the pack, it’s important to develop a compelling value proposition. A well-crafted value proposition articulates the unique benefits you provide and acts as...

Social media for Financial Advisors: 10 strategies for visibility

To build strong relationships with clients and prospects, financial professionals can benefit from having a strong online presence. Social media has become an effective way to create and nurture these relationships. This digital medium provides Advisors, Planners, and...

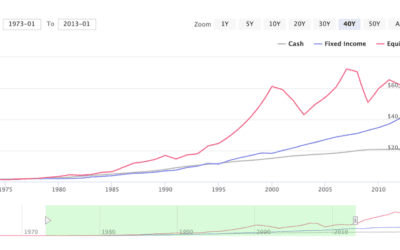

Use interactive charts to increase client engagement

Why client comprehension matters Interactive charts have become a cornerstone tool for Snap Advisors who want to educate their clients. Have you ever considered how much client comprehension and engagement impacts the financial plan’s chance of success? Ensuring your...

Financial Advisor podcast guide: top 24 shows in 2026

In an industry that evolves daily, successful Financial Advisors and Planners need to stay informed on market trends, practice management insights, and client behaviour. Podcasts have become one of the most efficient ways to do that—delivering expert analysis, diverse...

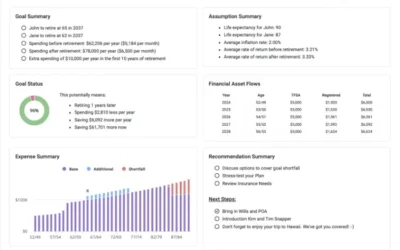

Create a customized financial plan report template in minutes

Today in our final session with Bill and Vicki Spicer, we are ready to move into the reporting phase of our planning. This 20-minute lesson will cover everything you need to know about building a client report from scratch, customizing that report, and saving your...

24 Financial Advisor questions to ask clients for better planning

Building strong client relationships goes beyond crunching numbers. Meaningful conversations help Financial Advisors uncover a client’s true priorities, long-term goals, and risk tolerance—allowing for more tailored and effective financial planning. By asking the...

Model Critical illness & Disability Insurance for your clients

Financial Planners, Investment Advisors, and Insurance Specialists can now wrap data-driven, personalized insurance recommendations into their financial planning with complete transparency. The Snap Product Team has done it again and we are thrilled to announce our...

Optimize retirement projections & improve client outcomes in 20 minutes

In this session, we are continuing from the previous lesson which covered the comprehensive initial scenario set-up. Today, we will continue from that initial plan creation and projection set-up to learn how we can now leverage the powerful planning pages, which are...

Financial Advisor Websites: Design Tips, Strategies & Examples

A well-designed website is more than just an online presence—it’s a vital tool for building trust and showcasing a Financial Advisor’s expertise. It serves as a digital front door, giving potential clients insight into your services and reinforcing confidence in your...

Learn how to build a spousal retirement plan in 15 minutes

Financial Planners and Investment Advisors are spending less time yet creating better financial plans—learn how in this short retirement planning tutorial. Efficient retirement planning During this session, you will learn how to run through the Scenario Setup section...

SEO for Financial Advisors: Boost traffic with these eight strategies

In the crowded Financial Services industry, standing out and attracting the right clients can be a challenge. A strong online presence can make all the difference, and search engine optimization (SEO) plays a crucial role in ensuring potential clients find your...

Advisors can model critical illness and disability insurance

We've got some exciting news to share—you can now model existing or proposed Critical illness and Disability insurance plans in Snap. 🙌 This has been a top demand from our Advisors and we are thrilled to have rolled this out. This is just phase 1, as more insurance...

Financial Advisor practice management: Five tools for growth

Running a successful Financial Advisory practice goes beyond offering sound financial advice—it requires efficient management, strong client relationships, and strict adherence to industry regulations. When operations are well-structured, Advisors can focus more on...

Answer Your Clients’ Top 6 Questions & Compare Options

During this 60-minute financial planning webinar, Canadian Advisors are learning how to compare options and optimize client outcomes. Top 6 financial questions clients have The focus of the session was to address what research indicates are the top financial questions...

29 Financial Advisor newsletter ideas to strengthen client trust

As a Financial Advisor or Planner, building strong client relationships is key to long-term success. Regular communication fosters trust, keeps clients engaged, and reinforces your role as a valuable resource. A well-crafted newsletter is one of the most effective...

Financial Advisor training: certifications, skills, and pathways

Becoming a successful Financial Advisor requires more than an interest in finance. As you know, it demands a commitment to lifelong learning, professional integrity, and client-focused expertise. In a field that evolves with new regulations, technologies, and market...

Provide better tax planning advice & improve clients’ tax efficiency

How can you provide better tax planning advice and improve your clients' tax efficiency? During this financial planning session, you will learn how to efficiently provide more in-depth tax optimization services to your clients. The most impactful components of this...

How Advisors Compare Scenarios to optimize client outcomes

Your clients have important financial questions that require personalized answers and recommendations. Common client questions For example: Should they purchase Corporately Owned Life Insurance? How can they reduce OAS clawback? Can they afford to retire earlier? Is...

One-page financial plan template: Key elements

When it comes to financial planning, clarity is key. Clients value concise, easy-to-digest information that helps them make informed decisions without sifting through pages of dense reports or lengthy presentations. That’s where the one-page financial plan comes into...

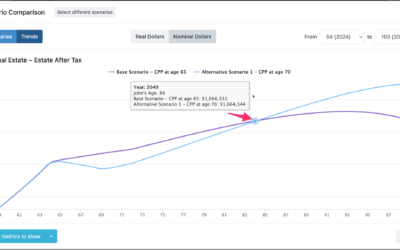

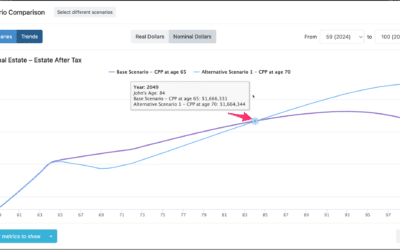

How Advisors answer client questions on government benefits

Would delaying CPP and OAS to ager 70 help our clients leave a larger estate for their children? As always, the correct answer is—it depends! Recent research has concluded that, "When evaluating RRIF strategies for a client, financial planners must take into account...

Understanding financial risk management for Advisors

A well-rounded financial plan considers both growth and stability. Clients look to their Advisors for insights as they make financial decisions, adjust to changing circumstances, and work toward their long-term goals. By incorporating thoughtful risk management...

17 powerful Financial Advisor marketing strategies

Attracting and retaining clients as a Financial Advisor takes more than just expertise. Because there are so many financial professionals, especially in larger cities or regions, a well-thought-out marketing plan can become necessary to generate leads and also convert...

Answer client retirement planning questions: Am I okay?

Advisors, learn how to answer client retirement planning questions during this financial planning tutorial. What questions keep your clients up at night? The most important retirement planning question—"Am I going to be okay?"—can be easily addressed with the right...

Estate Planning 101: The Complete Guide for Advisors

Estate planning is a delicate process for your clients, and, as a Financial Advisor, your role is to provide a clear and structured framework for addressing this complex topic. Since estate planning often involves discussions about legacy and support for loved ones,...

Advisors: build financial plans faster with automation

With Snap's automation features, Advisors can build financial plans faster than ever before. You can instantly provide personalized recommendations, compare options on a single page, and create a 1 or 2-page report instantly. In this financial planning tutorial for...

Retirement planning: Take the commuted value of my pension?

Today’s session is all about helping your clients retire with confidence. We are going to address the retirement planning question, “Is it better to take the commuted value of my pension?” Your clients have important financial questions that require personalized...

Retirement planning: A step-by-step guide for 2026

Retirement planning requires careful consideration of a few factors, including financial goals, risk tolerance, and anticipated lifestyle changes. While clients may have a general idea of their retirement aspirations, it is the Financial Advisor's responsibility to...

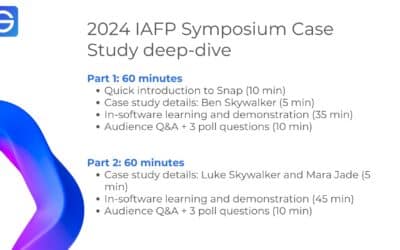

Provide clients with complex planning needs peace of mind

Snap Projections was thrilled to once again sponsor the annual IAFP Symposium. This year, the team conducted a Symposium Case Study deep-dive through a 2-part webinar series. The Case Study, May The Wealth Be With You, can be downloaded here. This case holds some...

Answer retirement income planning questions

Retirement income planning tutorial for Advisors In this retirement income planning tutorial, Advisors are working through a Case Study. Together, we are learning how to build a plan from scratch, create multiple what-if scenarios, and then discussing how to review...

New Scenario Comparison Feature

Instantly compare up to 5 scenarios with tables and visual charts. As an Advisor, you already know that the fundamental reason for creating multiple scenarios is to illustrate how they impact meaningful outcomes for your clients over time, and to help inform them of...

Introducing SnapShot: 1 Page Financial Plan Report

Transform the way financial advice is delivered with a 1 page report. With Snap, you’ve always been able to show your clients their whole life on one page. Now, you can create that same client experience using our newest reporting feature, the SnapShot — a 1 page...

3 Ways Advisors Can Personalize for Client Retention

If you want to retain clients long-term, personalization is key. But what exactly does that mean? And how can you provide it? In a recent article that was published by Investment Executive, Clients stick with advisors because of personalization: survey, it was...

Advisors Save Time & Delight Clients with SnapShot Report

On July 23, 2024, the team at Snap hosted this CE-accredited financial planning webinar that had 370 Financial Advisors & Planners register to attend. Live attendance was required to be eligible for the CE Credit. Watch the video. https://youtu.be/xhrfW4VP8Qk...

Top Canadian Financial Planner’s Growth Tips

On June 25, 2024, we sat down with Snap user Adam Bornn, CFP, CLU to discuss what practice management and practice growth strategies have been effective. Adam has been dedicated to clients looking to build financial, retirement, and estate plans since 2006. After...

What makes financial planning software effective?

What makes retirement projections software good? If you are like me, when you evaluate new software you are looking for specific features. You wonder: “How will this software take care of “X”? Or, “Can it help me with “Y”.

Engage Clients and Update Financial Plans Efficiently

Keeping your current Advisory clients engaged with the financial planning process can be a challenge. What are some ways Advisors can maintain the relationship, keep clients engaged, and ensure conversations remain current? How Advisors use Snap to engage their...

5 Lead Magnet Ideas for Financial Advisors

If you want make practice growth easier, it's time to start growing your email list with a Lead Magnet. Sending out regular emails of high quality content is a great way to stay engaged with current clients and to expand relationships. But how can you take this to the...

Email Marketing Template: Nurture Sequence for Advisors

In your basic 5-step process to start creating and sending out content via emails to your existing clients, we covered sending out a newsletter-style email on a regular schedule. Now, we can build on this idea once that has been established. What is a Nurture...

Financial Advisors Simplifying Corporate Planning

Have corporate planning discussions with confidence Ever wonder how other Advisors are simplifying corporate planning? Even if you are not currently providing corporate planning, you will still learn a lot during this financial planning tutorial. After watching this...

Save Time on Custom 1 or 2 Page Financial Plans

Do you absolutely love the report produced by your current Canadian financial planning software? If not, you may want to check out the newly released SnapShot feature by Snap Projections. Advisors can now provide their clients with a customized, one or two page...

Build a 1 Page Financial Plan Instantly

When customizability meets time savings The reports generated by financial planning software are too long. Even though Snap’s comprehensive reports are client friendly and easy to understand, the reality is that for many clients, even a 5-page report is still too...

15 Content Ideas to Attract Your Ideal Clients

One concept we have discussed previously when it comes to content creation is to always first start with the questions your current clients are asking. We covered this, and provided the steps to get started with content creation and email marketing in this article:...

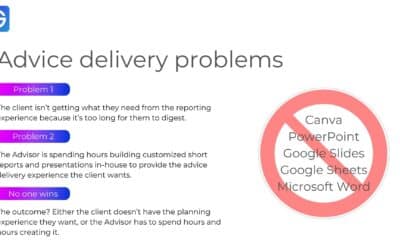

Transform Client Advice with a SnapShot Report

The 1 page financial plan summary report We recently announced the launch of the new SnapShot, Snap's latest major development. Advisors need and want better client reporting options. Period. Many of you are making short presentations in Canva or PowerPoint. This is...

Define Your Target Clients to Build Your Ideal Practice

Who do you want to serve? Building the practice you want takes time and concentrated effort. In the beginning, you may find it works to be more generalized with who you can help. But as your practice grows and evolves, at some point you will need to start making some...

Learn from top Advisor Jamie List, CFP

Learn from a top Canadian Advisor On March 6, 2024, Snap user Jamie List sat down with Snap Projections for an Advisor interview to share his background and depth of knowledge after working in the Canadian financial services industry for the last 30 years. Jamie is...

Efficiently Offer Personalized Planning for Clients

Personalization is key to client retention If you intend to keep your clients happy long term, providing personalized service is going to be essential. But how can you do that with efficiency? This tutorial tackled this challenge that many Advisors are dealing with —...

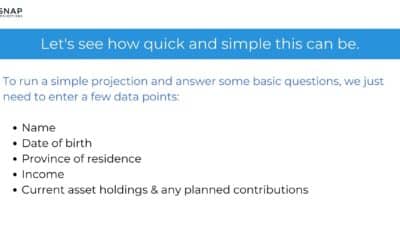

Create Projections in 5 Minutes with Snap Projections

In this video, you are going to witness how a basic financial plan can be built from end to end, in just 5 minutes using Snap Projections financial planning software. Watch the 5-minute financial plan build https://youtu.be/JTqPLnQSsMw Canadian Financial Advisors,...

Maximize Contributions: Advisor Tips

Advisors can do more planning with less data entry while helping their clients to see the value in maximizing TFSA & RRSP contributions. When you can show the personalized impact of what it looks like long-term to maximize contributions for your client, the...

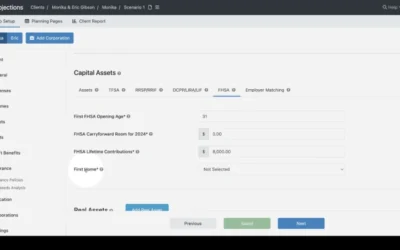

Model the FHSA: Cash-Flow & Goals Projections

As a Financial Advisor, Planner, or Investment Manager, how can you best help and prepare your clients for their futures? Every client, every case, is going to be completely unique. While yes, there will be commonalities and themes, what truly matters to each...

How Advisors Lose Clients: Expected Advice Not Delivered

If a client asks, how much more do I need to start saving in order to meet my retirement goals? and their Advisor can't tell them, it's a problem. If it takes them a long time to determine the answer, that's a problem, too. Advice expected but not delivered is how...

Financial Planning Software Tutorial: Complex to Simple

Here at Snap, we've always tried to keep things simple — especially when it comes to the use of our financial planning software. We've always pushed to ensure we keep it simple to use, but that does not mean sacrificing features and flexibility. Simple does not mean...

Grow The Advisory Practice: Networking & Partnerships

Networking and intentionally developing professional partnerships is crucial for individual business owners in essentially all industries, but for Financial Advisors, Planners, and Investment Managers, it can be really make or break. If you want grow the Advisory...

Grow Your Advisory Practice with a Referral Program

Providing exceptional service, encouraging client referrals, and implementing a Referral Program. Referral programs are a powerful strategy for Canadian Financial Advisors and Planners to grow their client base. Referral programs involve encouraging satisfied clients...

Engage Clients in Financial Planning: Start with a Vision

As a Financial Advisor or Planner, you already know how challenging it can be to get your existing and prospective clients engaged with the financial planning process. What we have found, in practice, is that starting with creating a retirement vision first can make...

Model the New FHSA in Snap Projections for Advisors

For individuals aiming to save for their first home purchase, the newly introduced First Home Savings Account (FHSA) offers substantial advantages. Financial Advisors, Planners, and Investment Managers who use Snap Projections told us that they wanted this new account...

Personalized Decumulation Strategies for Greater Value

When should your clients start taking CPP/QPP and OAS? Which accounts should they first draw from when they retire? Today we are going to explore personalized decumulation strategies. The answer is, it depends As a Financial Planner, you already know there are no...

Save Time & Boost Confidence with Financial Software

If you want to create more financial plans for more clients, saving time and increasing confidence are likely pretty high on your priority list. But — easier said than done? Only if you're not using the right tools. Advisors need to understand the numbers We speak...

4 Ways Referrals Boost Financial Advisory Community

In the ever-changing world of Financial Advisory services, differentiating from the competition while providing top-notch service to clients is paramount. One essential tool that has revolutionized the industry is financial planning software. Financial Advisors who...

Top Financial Advisors Increase Referral Rates

Top Financial Advisors, Planners, and Investment Managers continually refine and enhance their business operations and improving referral rates should be no different. The financial industry is marked by ever-evolving dynamics, including market shifts, regulatory...

Prepare Clients for the Unexpected

A Guide to prepare for the unexpected Let’s start with digging into the reasons why Financial Advisors and Planners should be helping their clients plan for the unexpected. The video case study addresses 4 specific client questions that are based on planning for those...

Start Creating Content in 5 Easy Steps

Creating content as a Financial Advisor or Financial Planner can be a highly effective way to engage with your audience, demonstrate your expertise, and attract potential clients. Let’s start with exploring the specific benefits to your practice, and then we can get...

4 Ways to Maximize Clients’ Money in Retirement

During the recording of this financial planning session, you will learn how to easily model 4 planning strategies that can have a major impact on your clients’ lives and retirement plans. You will see how addressing complex financial planning questions can actually be...

Proven Process to Convert More Prospects

We recently conducted a survey of Snap users and uncovered the three top business driving activities Financial Advisors, Planners, and Investment Managers are conducting with Snap's financial planning software. Are you currently prospecting? When we asked Snap users...

How Advisors Show Value and Impact Clients’ Lives

Financial Advisors and Planners can demonstrate value and positively impact their clients' lives in countless ways. Beyond merely providing financial advice, Advisors have the opportunity to build strong, trusted relationships with their clients and offer...

Cash-flow vs. Goals-based Financial Planning Software

Should your projections focus on cash-flow or goals-based planning? Cash-flow planning and goals-based planning are two distinct approaches to financial planning, each focusing on different aspects of an individual's financial situation and objectives. Ultimately, the...

New Expenses Module for Goals-Based Financial Planning

You asked, and we built it (again!) Goals-based financial planning We’ve just released a major product update; it’s something our users have been asking for — and it may be a functionality that your practice requires as well. It’s all about being able to dig deeper...

5 Easy Steps to Build Financial Plans for Clients

Experienced Financial Advisors can start doing more financial plans for their clients by following these 5 steps. Step 1: Review current client portfolios. Begin by reviewing your current client portfolios to identify clients who may benefit from a financial plan....

5 Ways to Engage Young Adults in Financial Planning

As an experienced Financial Advisor, Planner, or Investment Manager, you likely already know how important it is to start planning early for a successful financial future. Unfortunately, many young adults are not in that head space just yet and wind up missing out on...

4 Key Factors for Advisors When Choosing Financial Software

As a Financial Advisor, Planner, or Investment Manager, making the decision to switch financial planning software is almost never an easy one. There is much to consider, and every individual is going to have their own list of must-haves. We have spoken with thousands...

Engaging Financial Plans with Charts

When Financial Advisors are able to effectively present a financial plan, they can successfully engage clients in the financial planning process and cultivate long-term relationships. This is an important part of the process but something many Advisors tell us they...

6 Reasons Advisors Should Stress Test Clients’ Plans

By stress testing financial plans, Financial Advisors can help retirees identify potential risks, make informed decisions, and optimize their financial strategies to achieve their objectives and maintain financial security in retirement. Here are 6 of the top reasons...

Does Early RRIF Withdraw Benefit Canadian Retirees?

Retirement income planning research As Canadian retirees approach age 72 and have investments in a Registered Retirement Income Fund (RRIF), they are required to withdraw a minimum amount each year. However, some retirees may consider withdrawing more than the minimum...

How Corporate-Owned Life Insurance Boosted Estate Value

Case study on corporate life insurance Corporate-owned life insurance can be used as a tool not only to build wealth, but as an effective way to tax-efficiently transfer that wealth to beneficiaries. Corporately-owned life insurance policies can provide numerous...

Financial Planning’s Role in a Thriving Practice

The value in financial planning Do you have clients who don't see the value in planning? When your clients don't think they need a financial plan and you're having a hard time articulating the value, what can you do to help them understand? Learn what strategies 4 top...

Improve Corporate Financial Planning with Life Insurance

It's never been easier to provide tremendous value to your corporate financial planning clients. One easy way to improve corporate financial planning advice is through the modelling of life insurance. Snap now enables the modelling of corporate Whole Life and...

Stress Test Financial Plans for Clients

We know that right now inflation, interest rates, talk of bear markets, and declining portfolio values are top of mind for nearly all Canadians — in particular, those who are either approaching retirement or are already there. It's time to learn how to stress test...

Transparent retirement planning recommendations

As a Financial Advisor, you already know that your clients continue to demand more value in each and every client meeting. To start, they want transparent retirement planning. They want to understand where the numbers are coming from. To facilitate this, Advisors rely...

Tax Planning Tips for Financial Advisors

The Financial Advisor's Tax Planning Guide As you help your clients work through the many stages and phases of retirement income planning, financial planning, and creating long-term projections, the importance of tax planning undoubtedly remains a top priority and...

Boost Referrals with Snap’s Financial Planning Software

Welcome to Snap’s first ever user spotlight! Today, we’re doing a deep-dive with Renee Hawk. You can download the full case study down below if you want the numbers and business impact information. Let’s start with some questions.

Financial Planning for Business Owners: RDTOH Insights

Today, I'd like to share with you a few useful details on financial planning for business owners. Financial Planning for clients with corporations Integrating a holding company or an operating company into the personal retirement projections of your business owner...

Key Takeaways from the IAFP Symposium

The IAFP Symposium Recently I attended the IAFP Symposium in Vancouver, BC. It is one of the top conferences for Canadian financial planners and was, as always, packed with valuable content. I wanted to share with you the key takeaways from the conference, so you are...

Financial Planning Blog

If you’re a Financial Advisor and want to increase your client retention, check out our hub featuring expert insights, proven strategies, and industry best practices.

Get the Financial Planner's Toolkit

CRM3: Value is no longer shown by the return of your portfolio

The Canadian wealth industry is entering a new phase—one where transparency is no longer partial, and where performance alone is no longer enough to justify advice. Kaitlyn Lawson, head of practice management with CI Global Asset Management, was quoted in an article...

Double Your Time. Discover More Value. Snap Projections Is Offering a 30-Day Free Trial This August.

Snap's semi-annual promo is here Choosing the right financial planning software is an important decision. It isn't just about comparing features, it’s about finding a solution that fits naturally into your advice process, helps you deliver better client outcomes, and...

Income splitting in Canada: how it works, benefits, and implementation

Your client asks about income splitting during their retirement review. Suddenly, you are sorting through Tax on Split Income (TOSI) rules, attribution traps, and Canada Pension Plan (CPP) sharing. This resource will help you categorize client questions quickly,...

Permanent life insurance: types, benefits, and top policies

Permanent life insurance provides lifelong coverage with cash value growth. But moving from "what is it?" to "does it fit?" takes a clear breakdown, realistic cost anchors, and a walkthrough of what happens when clients tap cash value. This article will help you...

Why Financial Advisors Still Need Financial Planning Software in the Age of ChatGPT

Recent headlines have highlighted just how important it is for professionals to verify AI-generated information. In one widely reported Canadian case, legal professionals faced scrutiny after artificial intelligence generated court citations that simply did not...

Total Cost Reporting: What Advisors Need to Do Before 2027

The next major evolution in Canadian investment regulation is coming—and it will change how clients see cost, value, and advice. With the transition from CRM2 to CRM3 (also known as Total Cost Reporting, or TCR), Canadian Financial Advisors, Planners, and Investment...

Tech Rules for CFPs & QAFPs | FP Canada Standards Council

Did you know that there are new technology rules for Financial Planners? This blog post was originally published on October 28, 2021, and was last updated on June 17, 2026. In July 2021, the FP Canada Standards Council added two new rules to their Standards of...

AI-driven Financial Planning: Automate tasks & keep Advisors in control

Artificial intelligence seems to be everywhere right now. Every week, a new platform claims it can automate workflows, generate advice, replace manual processes, or completely transform the way Financial Advisors work. While there is certainly excitement around the...

Why the financial planning process is the most scalable growth strategy for Financial Advisors

For years, many Financial Advisory relationships have revolved around investment performance. But in today’s environment, especially with increasing fee transparency through Total Cost Reporting, clients are evaluating Advisors differently. They’re asking: What value...

Why Total Cost Reporting Is an Opportunity for Financial Advisors to Scale

For many Canadian Financial Advisors, the upcoming shift to CRM3—also known as Total Cost Reporting (TCR)—initially feels like a compliance burden. More disclosure. More scrutiny. More client questions. But that framing misses the bigger picture. CRM3 is not just a...

Term life insurance Canada: needs analysis steps for Advisors

Term life insurance Canada questions come up all the time. Even so, many recommendations still lean on outdated rules of thumb and quick "napkin math" that do not reflect a client's actual liabilities, timelines, and offsets. That is when coverage shifts mid-meeting...

New feature release: Automated Financial Recommendations

We are thrilled to announce that another much-anticipated feature is now live in Snap Projections. Financial Recommendations was created to automate the process of testing different optimization strategies in order to identify strong, practical and implementable...

CRM2 versus CRM3: What’s the Difference for Financial Advisors?

For Canadian Financial Advisors, regulation has steadily moved in one direction over the past decade: greater transparency. From the rollout of CRM2 to the upcoming implementation of CRM3, or Total Cost Reporting, the message from regulators is clear. Clients should...

How to calculate ACB: formula, table, and adjustments

Accurate capital gains reporting depends on adjusted cost base (ACB). But ACB tracking can break down when clients have reinvested distributions or return of capital. Broker statements often miss those adjustments, so you end up rebuilding ACB from slips, fund...

How Canadian Financial Advisors can save hours this tax season with ai data assist

Advisors can turn tax season into an opportunity with ai-powered data assist Tax season has always been a paradox for Financial Advisors. On one hand, it’s one of the most valuable times of year to deliver planning insights and deepen client relationships. On the...

After tax cash flow (ATCF): How to calculate, impact, & examples

Gross income does not tell the full story, especially when you are planning for retirement, big purchases, or long‑term cash flow needs. What really matters is how much money clients actually keep after taxes, deductions, and benefits are figured in. Understanding...

Managing a FHSA (First Home Savings Account): The guide

Buying a first home can feel out of reach, especially with rising prices and the need for a large down payment. But with the right plan, your clients can save faster while reducing their overall tax burden. Many Canadians don't yet realize how much the new First Home...

TFSA contribution limit: How to maximize clients’ savings

Many clients miss out on thousands in tax-free savings because they don't fully understand how the TFSA contribution limit works. Even small mistakes, such as re‑contributing too early or guessing contribution room, can lead to penalties or lost growth. As a Financial...

Financial Planning is hard enough—stop fighting with your software!

In today’s advice landscape, Canadian Financial Advisors are expected to deliver more than product recommendations. Clients want clarity. They want certainty. They want to understand how today’s decisions impact the rest of their lives. That’s where clear, fast, and...

Deliver more value this year with tax planning optimizations

Tax planning is no longer a “nice-to-have” conversation for Canadian Financial Advisors — it’s central to delivering real value. Clients don’t just want investment returns. They want to know: Are we minimizing taxes? Are we structuring this correctly? Are we leaving...

Reclaim Your Planning Hours with Snap Projections’ AI Data Assist

If you’re a Canadian Financial Advisor, you already know where too much of your week goes. Not in strategy. Not in meaningful client conversations. Not in refining recommendations. It goes into data entry. Investment accounts. Registered plans. Insurance policies....

Life insurance needs analysis: How to determine what clients need

Most families never expect financial hardship until it happens. The uncertainty your clients could face if an unexpected loss left them without a safety net can be scary to talk about. However, as the Advisor, you know it will be in your clients’ best interest to have...

Introducing Snap’s ai data-assist: No more manual data entry or errors

Turn client documents into usable plans—fast We are excited to announce that Advisors can now instantly build first drafts of financial plans using client documents with Snap's new data assist feature. Entering data manually is slow and error-prone. API and...

Corporate life insurance: How it works & key tax benefits

Many Canadian business owners don't realize how much risk they carry if a key person suddenly passes away. Losing a founder, owner, or critical team member can strain cash flow, disrupt operations, and create uncertainty, especially when insurance coverage is...

CPP enhancement: Purpose, implementation, and benefits

Retirement security in Canada is changing, and the CPP enhancement is at the centre of this shift. You may have heard about the updates, but knowing what they mean for you and your clients is important. The new CPP rules affect contributions, future income, and how...

RRIF withdrawal rates: What Financial Advisors need to know

RRIF withdrawal rates have a big impact on your clients' retirement income. The minimum amounts rise as clients get older, so Advisors need to understand how these rules work. This overview explains the key RRIF rules in a simple way. You will see how different...

OAS clawback: How it works, implications, & how to minimize risk

Many Canadians do not realize their government retirement benefits can decrease if their income gets too high. The OAS clawback lowers Old Age Security payments once clients pass a certain income level. You may be working with clients who are worried about losing...

Making the most of unused RRSP contributions: A guide for Advisors

Unused RRSP contributions can help clients when used the right way but they can also cause problems when they are not managed properly. Many Canadians do not know that these unused amounts can give them helpful flexibility in future years. Advisors who understand...

What is a defined benefit pension plan? A breakdown for Advisors

A defined benefit pension plan gives steady income in retirement. This type of pension can guide a client's choices for many years. Many Advisors know it is valuable, but the details can still be confusing. This article explains what a defined benefit pension plan is....

Retirement incoming planning optimizations to help your clients

September's retirement income planning webinar is a must-watch if your clients include pre-retirees. When your pre-retiree clients have questions, what is your process to provide answers and options? This lesson includes actionable retirement income planning...

Financial Planning for Younger Couples: Building a Strong Foundation With the Right Tools

Why young couples need a strong financial plan Starting life together as a couple is exciting—but it also comes with major financial decisions. From buying a first home, to raising children, to planning for retirement, the choices couples make early can shape their...

Advisors Can Help Clients Reduce Taxes by Moving Non-Registered Investments Into a TFSA

The problem with non-registered accounts Many Canadians accumulate wealth in non-registered accounts—whether through savings after maxing out RRSPs, inheritances, or simply because they haven’t been strategic about account types. While non-registered accounts are...

Why Advisors Should Conduct Personalized Insurance Needs Analyses

Why insurance planning deserves more attention Life, disability, and critical illness insurance are the foundation of many clients’ financial security. Without proper coverage, even the best-laid retirement or investment plans can be derailed by the unexpected. Yet...

This December Only: Double the Free Trial — Two Full Months of Risk-Free Planning with Snap Projections

December is a unique month in the world of financial planning. While markets slow and client meetings ease up, Advisors finally get one thing they rarely have during the busy year: time. And this year, that time is about to go even further. For December only, Snap...

Help Clients Make Smarter RRSP and TFSA Decisions with Personalized Financial Planning

Why personalization matters in financial planning One of the most common questions clients ask their Financial Planner or Advisor is:“Should I put money in my RRSP or my TFSA?” On the surface, it seems straightforward. Both are tax-advantaged savings accounts designed...

How Financial Planners and Advisors Can Save Time and Reduce Errors in the Planning Process

The challenge of time and accuracy in financial planning Financial Advisors and Planners wear many hats: strategist, coach, educator, and analyst. But two ongoing challenges come up in almost every practice: time and accuracy. Building financial plans can take...

Why Financial Planners Should Compare Multiple Scenarios to Optimize Client Outcomes

Financial planning is never one-size-fits-all. Each client has unique goals, challenges, and preferences. While one strategy may look strong on paper, it might not align with a client’s lifestyle or risk tolerance. That’s why comparing multiple scenarios is so...

Financial planning process: How to build & optimize plans in Snap

Snap Projections is designed to make financial planning faster, clearer, and more collaborative for Advisors and their clients. In this training series, we walked through every core feature—from setting up new clients and entering data, to customizing cash flow,...

How Taxable Income Targeting Helps Clients and Adds Value to the Financial Planning Process

For many clients, taxes are one of the biggest expenses they’ll face throughout life—especially in retirement. While saving and investing strategies are critical, effective tax planning can make just as much of a difference in preserving wealth. Yet many clients don’t...

One-page financial plan: template and checklist for 2026

Today’s clients expect financial advice that’s clear, visual, and actionable. Long reports can overwhelm—what they value most is a simple snapshot that connects their goals to a concrete plan. A one-page financial plan does exactly that. It condenses a client’s...

How Financial Advisors Can Provide Better Recommendations and Options to Clients

Financial planning isn’t just about crunching numbers—it’s about helping clients make confident decisions. Clients come to Advisors with big questions: When can I retire? How much can I spend? Am I saving enough? The most successful Advisors don’t just present data....

What financial planning questions do young couples have?

For young couples, financial planning starts with questions. For Advisors, each question is an opportunity to build trust and show value. By using Snap Projections in discovery meetings, you can move from uncertainty to clarity faster—helping couples see that...

How Financial Advisors and Financial Planners can convert more prospects

This CE-accredited webinar is about having better conversations that will increase client engagement & convert more prospects. This was filmed on Tuesday, July 22nd, 2025, at 1pm ET. Live attendance was required to be eligible for CE Credit. During the 60-minute...

Financial life stages: A guide for Advisors

Clients rarely reach major financial milestones by chance. Each life chapter, starting a career, raising a family, or planning for retirement, brings new priorities and decisions. Yet, many clients may not see these transitions coming, and even fewer may feel...

Provide better tax planning advice and improve your clients’ tax efficiency

This tax-focused financial planning webinar was filmed on June 24, 2025. Live attendance was required to be eligible for CE Credit. Comparing Scenarios for increased tax efficiency As we move into the case study, we’re going to be building out multiple scenarios that...

Trust and estate planning: key financial and legal considerations

Trust and estate planning is a crucial aspect of financial planning for Advisors and their clients, and it can be a very complicated topic. Whether your clients have a high net worth or not, it is important to engage with them while you help them navigate these...

The retirement checklist 101: Key steps to discuss with clients

Guiding clients through the complexities of retirement planning is a core part of your value as a Financial Advisor—a task made even more pressing by surveys that show over 75% of Canadians are worried they won't have enough money in retirement, highlighting the...

Cash flow analysis: how to prepare and explain concepts to clients

Advisors who want to provide clients with a comprehensive understanding of their financial situation must perform a cash flow analysis. This article addresses the importance of cash flow analysis for Financial Advisors and how professionals can effectively prepare...

The role of an Independent Financial Advisor: key responsibilities

Navigating the complexities of personal financial affairs can be challenging for clients, especially when they're just getting started. It's often hard to know where to begin, and there are so many factors to consider. How do they achieve their financial goals when...

Financial Advisor leads: top 14 strategies & tips for growth

Generating the right Financial Advisor leads is more than a numbers game—it's about connecting with people who truly need your expertise, yet a recent Deloitte report found that 78% of Advisors cite lead generation and referrals as their biggest growth hurdle. With...

How finfluencers are influencing client mindsets

You can find a finfluencer for nearly every financial topic, from investing in stocks to maximizing your RRSP to advanced cryptocurrency trading strategies. With just a few taps, Canadians can access financial commentary delivered through bite-sized videos, personal...

Wrap personalized insurance recommendations into your financial planning

This financial planning webinar is all about learning easy-to-execute strategies to help you wrap data-driven, personalized insurance recommendations into your financial planning with complete transparency. Please note: this session was recorded on May 20, 2025 and...

Why Financial Advisors Should Help Clients Maximize TFSA Top-Ups

Why TFSAs matter in financial planning The Tax-Free Savings Account (TFSA) has become one of the most powerful tools available to Canadian investors. With tax-free growth and tax-free withdrawals, it’s an essential vehicle for both short-term flexibility and long-term...

Top 12 Financial tech tools for growth in 2026

The financial landscape is evolving daily thanks to technology and the emergence of savvy investors seeking personalized, tech-driven financial solutions. Recent McKinsey analysis indicates that adoption of generative-AI tools can save Advisors time, underscoring how...

Stress testing in risk management: what you need to know

Uncertainty is one of the biggest challenges in financial planning and business management. Market downturns, inflation spikes, sudden income loss, or unexpected operational disruptions can derail even the most carefully built strategies. For Financial Advisors and...

Decumulation strategies: A guide to retirement income planning

Retirement planning is more than just saving for the future — it’s about strategically using those savings to sustain a fulfilling and financially secure lifestyle. This process, known as decumulation, involves transitioning from building wealth to effectively...

Cash flow projection template: What it is and how to use it

Financial Advisors regularly create financial plans to help clients achieve their goals. To do this effectively, they need to invest time and effort to understand each client’s unique financial situation, including their objectives, risk tolerance, and capacity. Once...

What is scenario analysis? Benefits, types, and examples

Preparing for the future is rarely simple. Uncertainty is a constant, and the most effective strategies are those that embrace flexibility and plan for the unexpected. Scenario analysis provides a robust framework for evaluating possible outcomes, anticipating...

How to get clients as a Financial Advisor: 7 proven ways

Whether you're building your book of business or expanding an established practice, bringing in new clients often presents a meaningful challenge for Financial Advisors. In a landscape that includes robo-advisors, financial influencers, and a constant stream of...

Financial planning steps: The ultimate guide for Advisors

Clients today seek more than generic advice; they are looking for clarity, control, and a plan they can trust. Yet many underestimate the value that comes from a truly personalized financial roadmap. As a Financial Advisor, following a clearly defined planning process...

Goal-based financial planning: A practical Advisor guide

Financial Advisors are often on the lookout for strategies that deepen client relationships, create an environment of trust, and genuinely connect financial actions to a client’s life plans and goals. Goal-based financial planning is a powerful methodology that...

High-net-worth clients: Definition, criteria, and growth strategies

Serving high-net-worth (HNW) clients represents a significant opportunity for Financial Advisors and Wealth Managers. This discerning segment with substantial investable assets and intricate financial lives demands a highly personalized approach to wealth management....

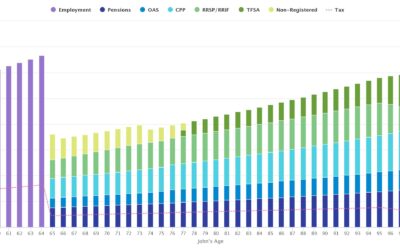

Automated Taxable Income Targeting [new feature update in Snap]

Effectively managing contributions and withdrawals to maintain a specific taxable income and marginal tax rate can have a profound impact on reducing your clients’ overall tax burden—both in the short term and over the course of their retirement. With Snap’s new...

Financial Advisor business plan: A guide to going independent

Starting an independent Financial Advisory practice can be both exciting and challenging. Many Advisors pursue independence to gain more control, build stronger client relationships, and shape a business that reflects their values. Making the move from employment to...

16 Financial Advisor interview questions to hire top talent

The quality of your Financial Advisory team directly impacts your firm's growth, reputation, and ability to deliver exceptional services. An effective hiring process can ensure that your firm is staffed with capable professionals and has a client-centric culture that...

10 client rapport strategies to grow your financial practice

Building long-term relationships with clients is one of the foundations of a successful practice in the financial services sector. Advisors and Planners who focus on building strong client relationships are often in the best position to improve client retention, earn...

Financial advertising: Strategies, trends, and regulations

Attracting the right clients and growing a sustainable practice requires more than technical expertise—it takes clear, consistent communication that reflects your values, process, and professionalism. Today, prospective clients often assess a Financial Advisor’s...

Managing client expectations: A guide for Financial Advisors

Helping clients form realistic and informed expectations is an important part of effective Financial Planning. While investment strategies and portfolio management play a role, much of an Advisor’s value also lies in supporting clients as they navigate financial...

What is holistic financial planning? Key principles explained

Financial planning is evolving and has shifted from product-focused conversations to more personalized, client-centred approaches. Today’s clients are looking for strategies that reflect not just their finances, but also their values, goals, and life experiences. In...

Client onboarding: Steps to build trust for Financial Advisors

The initial interactions a Financial Advisor has with a new client are critical. This period, known as client onboarding, sets the foundation for what will hopefully become a long and mutually beneficial relationship. A well-structured and thoughtful onboarding...

Advisory Team leadership: How to guide and grow your team

Leading an Advisory Team involves more than task delegation—it’s about fostering a collaborative environment where team members can do their best work and deliver meaningful value to clients. As client expectations shift and practices grow, effective leadership plays...

14 essential Financial Advisor skills & how to develop them

As you know, a Financial Advisor’s duties go beyond the number-crunching aspects of their role. To build strong client relationships and deliver long-term value, Advisors often benefit from a mix of technical knowledge and interpersonal strengths. In this article, we...

Best sales training for Financial Advisors: Courses & tips

Financial Advisory is a relationship-driven profession where lasting success often stems from earning trust and communicating value clearly. While the word “sales” may carry traditional associations, in the context of Financial Planning, it’s less about persuasion and...

Creating a Financial Advisor value proposition: 10 effective tips

As a Financial Advisor, Planner, or Investment Manager who wants to differentiate themselves and stand out from the pack, it’s important to develop a compelling value proposition. A well-crafted value proposition articulates the unique benefits you provide and acts as...

Social media for Financial Advisors: 10 strategies for visibility

To build strong relationships with clients and prospects, financial professionals can benefit from having a strong online presence. Social media has become an effective way to create and nurture these relationships. This digital medium provides Advisors, Planners, and...

Use interactive charts to increase client engagement

Why client comprehension matters Interactive charts have become a cornerstone tool for Snap Advisors who want to educate their clients. Have you ever considered how much client comprehension and engagement impacts the financial plan’s chance of success? Ensuring your...

Financial Advisor podcast guide: top 24 shows in 2026

In an industry that evolves daily, successful Financial Advisors and Planners need to stay informed on market trends, practice management insights, and client behaviour. Podcasts have become one of the most efficient ways to do that—delivering expert analysis, diverse...

Create a customized financial plan report template in minutes

Today in our final session with Bill and Vicki Spicer, we are ready to move into the reporting phase of our planning. This 20-minute lesson will cover everything you need to know about building a client report from scratch, customizing that report, and saving your...

24 Financial Advisor questions to ask clients for better planning