Snap Projections vs RazorPlan: Choosing the Right Financial Planning Software

Canadian Financial Advisors comparing Snap Projections vs RazorPlan need to understand key feature differences that impact their planning capabilities. While RazorPlan focuses on simplicity, many Advisors discover this approach creates limitations when clients need personalized scenarios or comprehensive planning.

Snap Projections provides the flexibility and advanced features Canadian Advisors need without sacrificing ease of use.

Snap Projections vs RazorPlan: What Canadian Advisors Need to Know

When evaluating Snap Projections vs RazorPlan, the choice comes down to feature depth versus simplicity. RazorPlan keeps things streamlined but lacks critical capabilities that Advisors need for comprehensive planning. Snap Projections delivers advanced features like multiple account type entry, customizable withdrawal strategies, and real-time scenario modifications that RazorPlan simply doesn’t offer.

Feature Comparison: Snap Projections vs RazorPlan

Snap Projections |

RazorPlan |

|

| Create simple projections in 20 minutes or less | ✔ | ✔ |

| Scenario-specific Recommendations | ✔ | ✔ |

| Stress test your projections with historical or randomized returns | ✔ | ✔ |

| Retirement income planning | ✔ | ✔ |

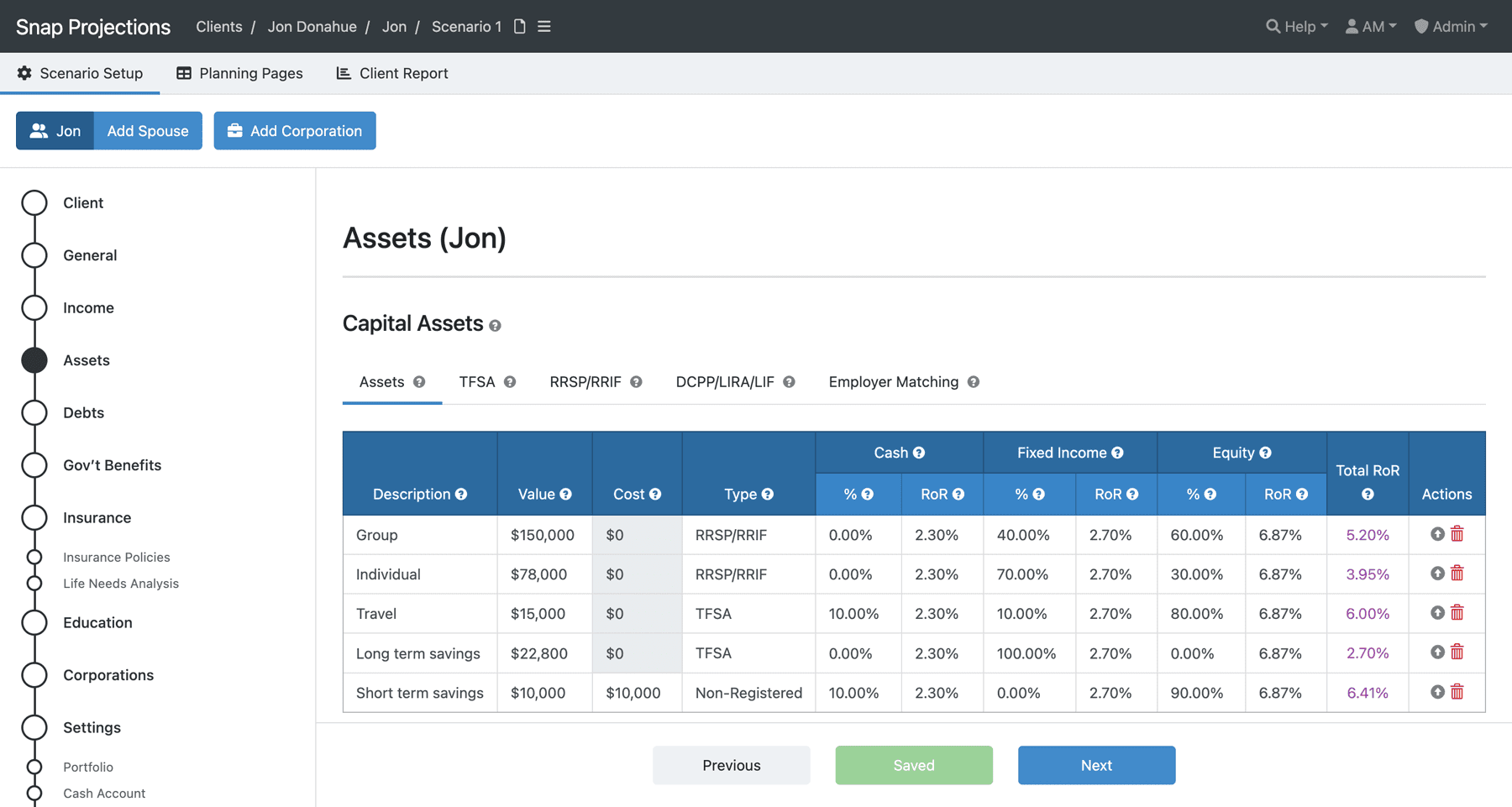

| Enter multiple accounts of the same type (e.g. 2 or more RRSPs, TFSAs, LIRAs, Non-reg) | ✔ | |

| Ability to enter the actual withdrawal amounts for Non-Registerd, TFSA and LIFs. | ✔ | |

| Create multiple "what-if" scenarios for comparison | ✔ | ✔ |

| Modify scenario data (income, contributions, withdrawals, rates of return, etc.) from a single Planning Page | ✔ | |

| Client friendly reporting | ✔ | ✔ |

| Automated & fully optimized income splitting for every year of the projections | ✔ | |

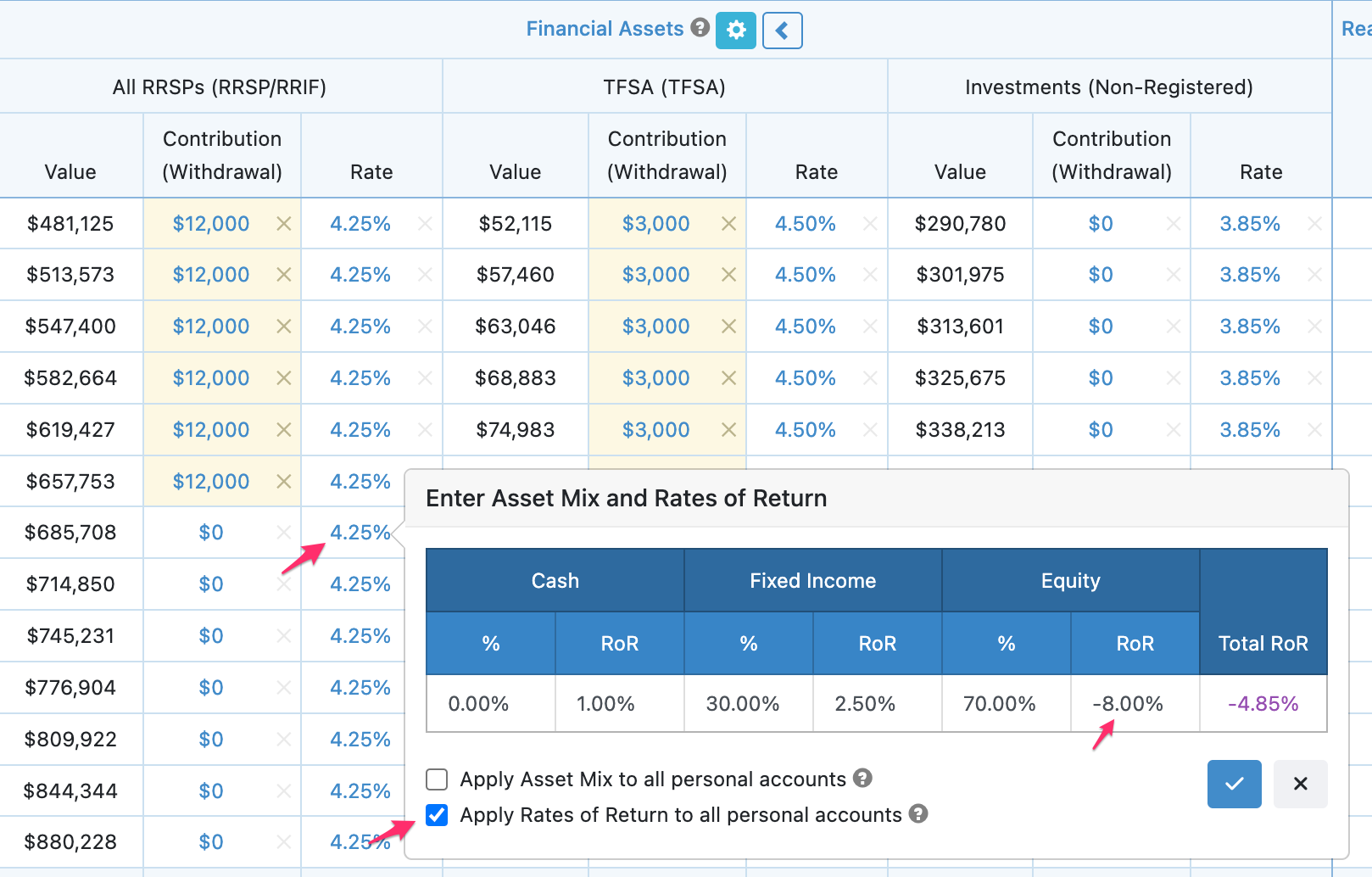

| Ability to set custom asset allocation for individual accounts | ✔ | |

| Life insurance planning | ✔ | ✔ |

| Highly customizable critical illness and disability insurance recommendations | ✔ | |

| Dedicated charitable donations module for cash, assets & insurance | ✔ | |

| Monthly & annual plans available | ✔ | ✔ |

| Enterprise capability | ✔ | ✔ |

| Data security & compliance | ✔ | ✔ |

Try Snap Projections for Your Practice

Feature Gaps Between Snap Projections and RazorPlan

Analysing Snap Projections vs RazorPlan requires Canadian Financial Advisors to examine how these systems handle information input, taxation analysis, and client communication to identify which platform aligns with their practice requirements.

These feature limitations in RazorPlan create real challenges for Canadian Advisors who need comprehensive planning capabilities.

Multiple Account Entry - RazorPlan Forces Account Consolidation

Snap Projections lets you enter accounts individually or combine them—giving you the flexibility to accurately model your client’s account structure and create specific withdrawal strategies for each account.

Limited Withdrawal Control in Decumulation

Snap Projections provides complete year-by-year control over all account types. Set custom withdrawal amounts, create withdrawal logic, and adjust strategies directly from the main planning page.

No Real-Time Scenario Modifications

Snap Projections enables instant scenario changes from one planning page. Adjust contributions, retirement dates, or inheritance amounts with a few clicks while maintaining client engagement throughout the conversation.

Restricted Asset Allocation Settings

Snap Projections allows custom asset allocation for each account, enabling accurate tax calculations and realistic investment projections that reflect your client’s actual portfolio structure.

Limited Tax Planning Access

Snap Projections displays tax information directly on the main planning page with one-click access to detailed breakdowns. Make RRSP contribution adjustments and instantly see tax implications without leaving the planning screen.

Inflexible Report Customization

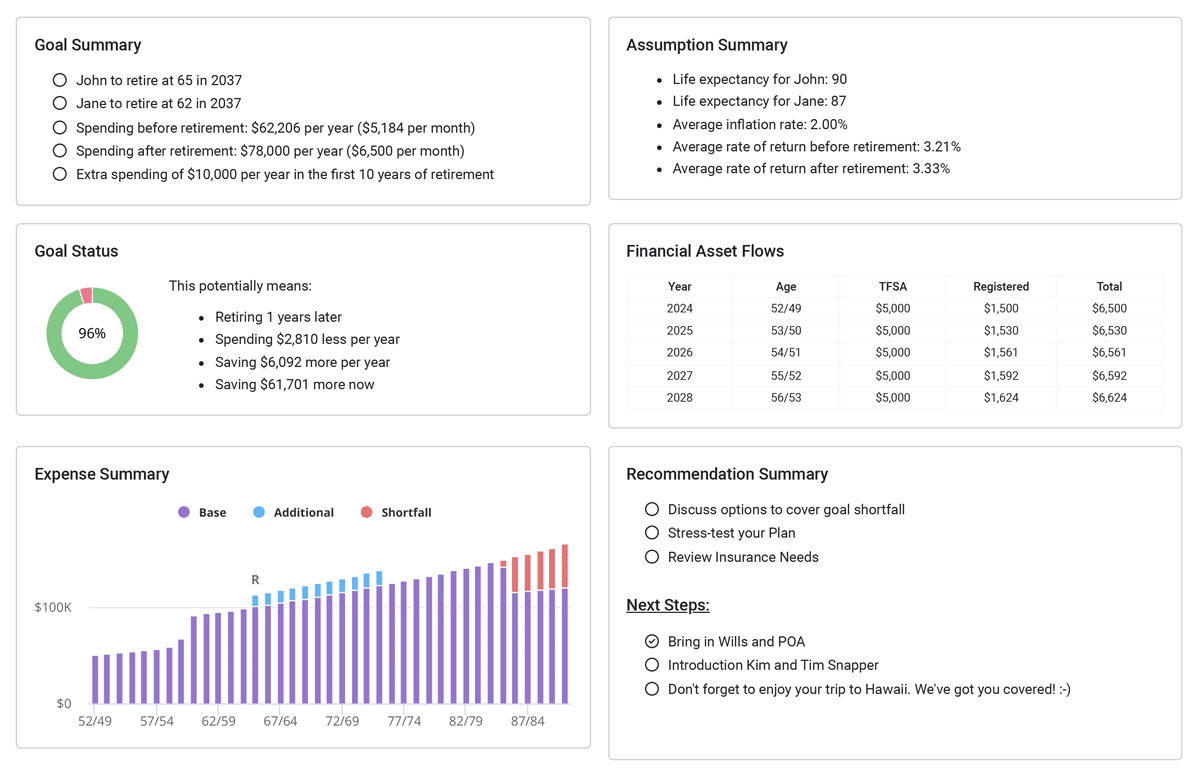

Snap Projections allows complete report customization including personalized recommendations, goals, and comments in each section, plus branded formatting that reflects your practice.

Read our financial planning software reviews on Capterra

See Why Advisors are Switching from RazorPlan to Snap Projections

“I’m really loving Snap! I was using Razor in the past, but really prefer Snap. I have a real mistrust of technology, and if I can’t see where the numbers are coming from, it makes me very uncomfortable. I am very impressed with how your program lays out the numbers, and how easy it is to make changes and double check for accuracy.”

“Snap has really streamlined my client conversations. With other software, I would have to collect the data, then need to take that back and work in the program on my own, and then have a 2nd meeting to present. I wasn’t able to work efficiently within the program to do it in front of a client. With Snap, the client and I can work together on the data, and get it all done in one appointment, cutting the number of meetings required in half. The process just simply flows better.”

Clients, Partners & Affiliations

Find out why Advisors say Snap Projections is the top choice for individual Advisors and small to medium Advisory practices.

Frequently Asked Questions

What features does RazorPlan lack compared to Snap Projections?

RazorPlan lacks several critical features Canadian Advisors need: multiple account entry (e.g. forces consolidation if there are multiple TFSAs), custom withdrawal and contribution control for all accounts, real-time scenario modifications from one page, individual asset allocation settings, and accessible tax planning information. These limitations make comprehensive planning difficult when clients need detailed strategies beyond basic retirement projections.

Can I enter multiple RRSPs or TFSAs in RazorPlan?

No, RazorPlan only allows one account per account type, forcing you to combine multiple RRSPs, TFSAs, or non-registered accounts during setup. This creates problems during decumulation when you need different withdrawal strategies for separate accounts, requires manual calculations to consolidate, and creates confusion for the client Snap Projections allows unlimited accounts of each type, matching your client’s actual account structure.

How accessible is tax information in RazorPlan vs Snap Projections?

RazorPlan stores tax details in separate ledgers requiring navigation away from the main planning area, making tax planning conversations difficult. Snap Projections displays tax information directly on the main planning page with one-click access to detailed breakdowns and instant updates when making contribution changes.

Does RazorPlan allow custom withdrawal strategies?

RazorPlan has limited withdrawal customization—you can only modify registered and corporate account withdrawals. TFSA and non-registered account withdrawals are automatically calculated by the software with no option for manual adjustments. Snap Projections provides complete control over withdrawal amounts and strategies for all account types.

Can I make real-time changes during client meetings in RazorPlan?

RazorPlan requires navigation through multiple pages and verification of settings each time you modify a scenario, making real-time changes during client meetings difficult. Snap Projections enables instant scenario modifications from one planning page, allowing you to adjust variables while maintaining client engagement.

Which platform offers better customization for Canadian Advisors?

Snap Projections offers significantly more customization than RazorPlan. While RazorPlan prioritizes simplicity, it lacks flexibility for complex client situations. Snap Projections provides multiple account type entry, custom asset allocation, flexible withdrawal strategies, accessible tax planning, and customizable reports while maintaining ease of use for Canadian Advisors.