Top Financial Advisors, Planners, and Investment Managers continually refine and enhance their business operations and improving referral rates should be no different.

The financial industry is marked by ever-evolving dynamics, including market shifts, regulatory updates, and advancements in technology. Staying ahead (or at least trying to keep up!) of these changes is essential for remaining competitive and relevant in a rapidly changing landscape. Things are changing now faster than ever before and that pace is likely to continue.

The change is constant

Further to that, client expectations are constantly evolving. To provide superior service and maintain client satisfaction and retention, Advisors need to consistently enhance their own service offerings to meet and exceed changing client needs. Adapting to changing client preferences is essential if you want to build long-lasting client relationships.

Technology also plays a major role in the modern financial sector. Embracing technological innovations can significantly improve operational efficiency, streamline processes, and enhance the overall client experience.

To stand out and not only maintain but grow their practices, top Financial Advisors must continually refine their processes, differentiate themselves, and find unique value propositions that set them apart from other financial professionals. Ongoing refinement and enhancement of Advisory practices are essential for ensuring the long-term success of your business.

As a Financial Advisor, Planner, or Investment Manager, you already know the value of referrals to your practice. It turns out that this is also one of the easiest areas you can refine, optimize, and improve for significant long-term results.

The Referability Quadrant

A few years ago, we wrote about something called the The Referability Quadrant: How top financial advisors grow their advisory practices. It is these same 4 quadrants we’re going to explore more in-depth today.

Download your free digital marketing guide for Canadian Financial Advisors, Planners, and Investment Managers here.

Here are the 4 ways you can increase your Financial Advisory practice’s referral rates.

Elevate your practice

There are countless ways you can leverage technology to elevate your practice. Here are two of the most impactful ones that have become widely accepted these last several years. These two are now more important than ever because clients have been given a taste, and they now have a preference. What that preference is, however, will be unique to each individual and up to you to figure out.

Shift to Online Meetings:

Implementing online meetings is a game-changer. Jason Pereira, Partner & Financial Planner at Woodgate Financial, Inc., discovered this firsthand years before COVID forced the hands of many into this practice. His team used to spend nearly 70% of their time manually scheduling and confirming appointments with clients over the phone. By transitioning to an online solution to automate this process, they dramatically reduced appointment scheduling to just 20% of their staff member’s day. This liberated time for more productive tasks and improved operational efficiency. Clients also benefit from easily selecting appointment times without the hassle of phone tag.

As many teams are now returning to the office, we need to ask ourselves — do clients want to follow suit? An ideal approach, as many transition back to in-person meetings, may be to give your clients the option to have an in-person or online meeting. Their answers may surprise you!

Embrace Face-to-Screen Technology:

The advent of face-to-screen technology is revolutionizing the financial advisory landscape. Many Advisors are learning that sometimes even clients living in the same town prefer online meetings simply for the time-saving. Respecting your clients’ time demonstrates your commitment to prioritize their needs, making you more referable. Zoom and Microsoft Teams have proven to be great tools for this.

As it turns out, top Advisors were employing these practices long before they had to.

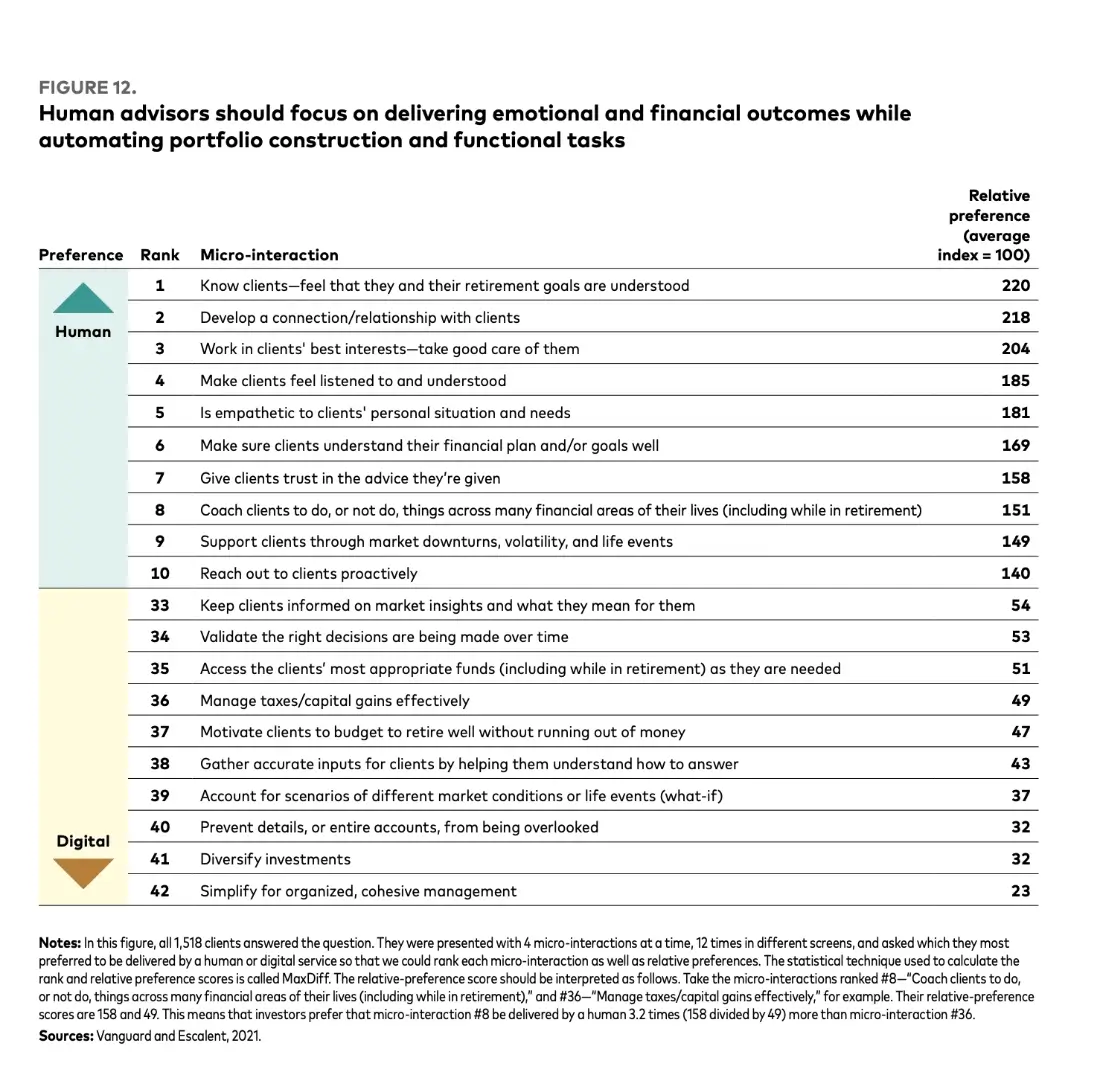

What do clients want delivered in-person?

It is important, however, to carefully consider where the human element matters and where your clients may be happy to substitute with technology.

One Vanguard study that explored this subject found that what clients value most from their Advisors are often intangible things like feeling heard, having a trusted relationship, and feeling supported. In this study, clients were asked about their preferences regarding the means of receiving specific Advisory services, whether through human interaction or digital platforms. Predictably, some investors leaned towards human delivery for most services, while others favoured digital methods. However, the interesting piece here is that these preferences were not uniform across all services.

Understanding these relative preferences for service delivery holds significant importance for two key reasons.

Firstly, it assists Advisors in fine-tuning their services to match the right clients according to their service model. Advisors need to be mindful of their overall cost-to-serve model and acknowledge that not all delivery channels may suit every client as they segment their business.

Secondly, given that an Advisor’s time is a limited resource, having a grasp of which services can be automated allows for the efficient scaling of their practices while keeping costs in check.

The key take-away here is that some things can be provided digitally while others cannot.

Vanguard study results on financial planning and the delivery of service

Engage Your Prospects

According to some experts, top Advisors focus on client engagement over customer experience in their financial planning process. Paulo Sironi, a leading figure in FinTech, emphasizes that customer experience can be copied or purchased, losing its competitive edge. To stand out, you need to offer real value to prospects.

Financial planning offers an excellent way to engage clients, providing them with predictable value. Before recommending products, financial plans should be the cornerstone of your client relationships. Understand your clients’ financial concerns, whether it’s home improvements, saving for their children’s education, or retirement. Asking insightful questions and empathetic listening are key. By aligning with their life goals, financial aspirations, and challenges, you become an essential part of their life, fostering long-lasting relationships and naturally leading to referrals.

Some Advisors may not feel they have time to engage with prospects in the financial planning process, but there are proven ways to do this efficiently. One way is to use financial planning software to show them what it looks like to work with you. With the right tech, you can use just a few key pieces of information to engage prospects and start answering their financial questions. You can almost instantly start providing value before asking for anything in return.

In this article and video case study, Financial Advisors: Here is a proven process to convert more prospects, you will see how much value can be provided with 5 pieces of data.

In this case, we are only using the prospect’s:

- date of birth

- Province of residence

- Income (estimate is fine)

- Existing capital assets (estimate is fine)

- Planned contributions (estimate is fine)

If you can give someone ten minutes, that’s enough time to get them excited about seeing more. Once they become excited about the financial planning process, collecting the rest of the information you need becomes much easier. Trust is already being built because you are leading with providing value.

Educate Your Clients

Research demonstrates that clients are more likely to refer their Advisors as their financial literacy levels increase. Investing in client education is not only beneficial for serving and retaining clients but also for growing your practice.

Some ways to increase client education include:

- Avoid lengthy, textbook-style financial plans. Instead, offer practical education on the specific impacts of financial decisions.

- Address clients’ primary concerns about their finances.

- Explain the consequences of following your advice versus staying the course.

- Clarify the longevity of their assets in retirement and when to claim government benefits.

- Prioritize practical “what-if” scenarios to enhance understanding, build trust, and encourage clients to share their newfound knowledge with others.

Snap Projections has interviewed over 3,000 Financial Advisors, Planners, and Investment Managers and this research has indicated these are the top 6 questions clients need answers to.

- How long will my money last? Am I going to be okay?

- How much can I spend in retirement?

- When should I take my government benefits?

- Which of my assets should I spend first?

- Am I saving enough?

- How much will be left for my kids and other beneficiaries?

Finding an efficient way to address these questions is one of the simplest ways to begin educating your clients.

If your client-base is younger, here are 5 Ways To Get Your Clients’ Adult Children & Other Young Professionals Engaged with Financial Planning.

Evaluate Your Systems

To maintain a competitive edge, create a feedback loop to identify areas for improvement.

As Peter Drucker once said, “What gets measured gets improved.”

Measuring results and seeking feedback from clients should be a regular practice. Surprisingly, setting up a client feedback system can also yield referrals if implemented correctly. Many industry experts have developed systematic referral-gathering processes. By incorporating feedback and referrals into your evaluation process, you can harness a significant opportunity that many Advisors overlook.

It’s good to start with a benchmark before making any changes so you can measure the impact. Are you averaging one referral each month, or five? Learn how one Advisor tripled her monthly referrals here.

Getting started with collecting client feedback can be as simple as sending a survey to your existing clients, which is something discussed in this Financial Advisor Panel on using a Financial Planning process to build a sustainable & thriving practice.

By focusing on these four areas — elevate, engage, educate, evaluate — you can position your Advisory practice to maximize referrals and, most importantly, assist more people in achieving their financial goals. After all, the ultimate goal is to help Canadians make better financial decisions.