The Financial Advisor’s Tax Planning Guide

As you help your clients work through the many stages and phases of retirement income planning, financial planning, and creating long-term projections, the importance of tax planning undoubtedly remains a top priority and focus throughout these discussions. Whether you’re a Financial Planner, Advisor, or an Investment or Wealth Manager, chances are that your clients are coming to you for financial and retirement planning advice.

At its core, a solid tax planning strategy will have invaluable long-term benefits for your clients. It will ensure that there are no unnecessary taxes being paid during the asset decumlation phase, help to keep investments efficient, provide ample opportunities and insights for charitable donations, maximize both your clients after-tax spending and estate value … I could go on, but I think you get the picture so I’ll stop there.

Likely, you already know all of this — the real issue here is how to facilitate, implement, and execute these tax planning conversations without creating additional work in your already jam-packed schedule. The good news is that this is the very objective of this blog post — to help you provide tax planning through your financial advisory process in an efficient and streamlined way.

Asset decumulation

Asset decumulation is a major component of retirement income planning and it rarely gets the attention it deserves. Everyone talks about saving and investing but no one ever talks about the best way to spend during retirement.

As a financial planning tool, Snap’s primary objective is to maximize the longevity of your client’s portfolio by minimizing or deferring tax liability, thus providing them with the highest possible amount of after-tax spending throughout their retirement or the highest after-tax estate.

Snap’s default logic to maximize your client’s resources during retirement is to first drain the non-registered accounts, followed by the TFSAs, and then the registered accounts, outside of any RIF or LIF minimums. This will keep marginal tax rates as low as possible during the early years of retirement.

In some cases, this strategy won’t align with your clients’ objectives so it’s simple to create your own decumulation strategy by setting your own default (we call this the cash flow management logic).

Additionally, you can make manual overrides to the default withdrawals.

Decumulation: which way is optimal?

This is a simple question on the surface, but the answer isn’t always obvious. We would need to define the client’s goals first.

For instance, are we optimizing for the:

- Highest retirement income?

- Highest estate value?

- Lowest estate taxes?

- Short-term liquidity?

- Long-term growth?

You can access Snap’s Recommendations feature to explore further optimizations and ideas:

We suggest using this Financial Planning Questionnaire with your clients to ensure you fully understand their needs, goals, dreams, and desires. This knowledge is what will put you in the position to truly help them. Plus, it makes your data entry much easier. You do not need to be an existing Snap user to take advantage of our questionnaire.

| Between the default CFM logic, and the pension income splitting, Snap Projections does perform initial optimizations on the order of withdrawals, and for 90% of cases, the defaults work very well. |

However, you can modify the default algorithm (to essentially create your own default logic) and achieve even more desirable results. You can use the CFM Order column to change the order around and see if that results in either a higher cash flow or higher estate value, depending on the goals of the client. As well you can change the conversion age for RRSPs and LIRAs, and see whether drawing the minimums sooner or deferring them until later creates a better outcome.

In most cases, the defaults work great for quick planning. However, if you want to invest some time optimizing for a specific goal, you can create copies of the base scenario and see if changing the default settings yields a more favourable outcome for your client.

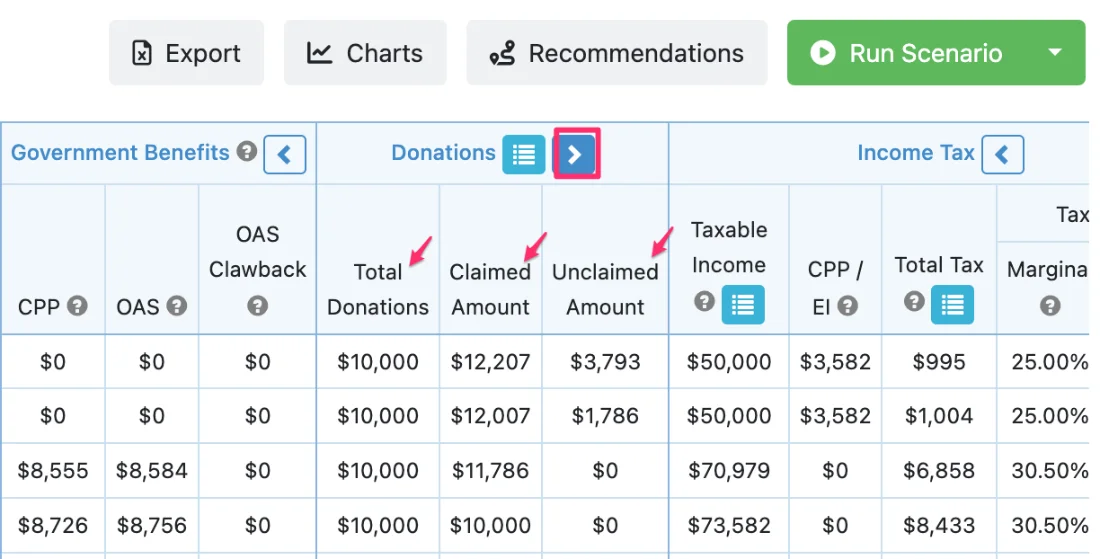

Charitable donations

Planning for charitable donations is an essential part of both tax and estate planning — modelling the impact of any potential decisions for your clients not only provides them with a massive value with respect to tax planning, but will help ensure their legacy dreams become reality.

In Snap Projections, you can easily plan for assets, insurance, and cash donations and have the associated tax credits applied to your projections. You can see the guide on that here.

Tax credits, deductions, & taxable benefits

In Snap, entering these critical pieces of the tax planning pie is simple. You can see the step-by-step guide in our help section that will help you set those things up to ensure each plan is totally customized for your client.

Maximizing RRSP & TFSA contributions

Unused RRSP and TFSA contribution room is tracked and shown easily in Snap to ensure your clients are leveraging those opportunities. You can see the breakdown of how those calculations are done here and what assumptions the software starts with.

If extra funds are being invested or saved during the decumulation phase, Snap’s default logic will be to maximize for tax efficiency, automatically maximizing first the RRSP and then the TFSA. The software does the calculations for you, and you can easily modify the default logic and create your own decumulation and contribution strategy as well.

Spousal situations

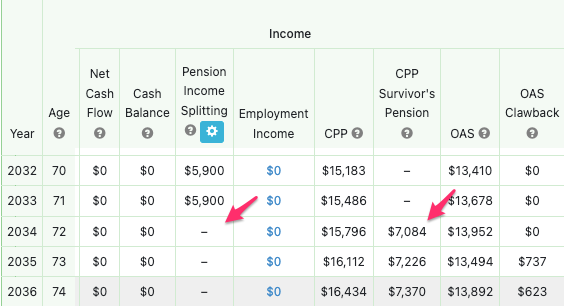

When you’re dealing with spousal scenarios, Snap is going to do all the heavy lifting for you. You have all the advanced options you need to optimize the situation with easy access to elements like pension income splitting and even basing the minimum RRIF withdrawals on the age of the younger spouse.

You can easily set up a spousal RRSP or model a surviving spouse scenario (that includes asset rollover) by simply modifying the projection length for one person. It really is that simple to show your clients what their financial situation could look like if one spouse passes away earlier than expected.

Transparency and compliance

We spend a lot of time talking with our users, as our product truly is a user-led design. Our product team works continuously to improve, iterate, and build the new features our current users are requesting.

One thing we know first hand is that lack of transparency and hidden calculations is an absolute deal-breaker for Financial Advisors, especially when it comes to tax planning. If your client pushes back or asks a question, you need to be confident with what you’re presenting and you need to know you’ll be able to not only answer their questions but explain how the numbers were generated. If you’re a CFP or QAFP, your designation requires that you understand how the software you’re using for financial planning works. You can read more on those rules here.

This is exactly why you will find tax tables to show you what is under the hood and behind those high-level numbers on the main planning page. You can see what those look like and how the calculations are generated right here. And, we make it easy for you to export these tax tables and entire spreadsheets into Excel, should you need to pull the information out of the software for your own verification purposes.

With respect to compliance, we provide multiple resources to help cover you. Our Financial Planning Questionnaire can help you satisfy your KYC requirements, and our reports provide a full summary of key values for the plan (including our Life Needs Analysis tool) to share with your clients.

All assumptions are included within the report for complete transparency and documentation purposes.

Updating last year’s plans

Updating old plans can be cumbersome, but it doesn’t have to be. With Snap, you’ll be able to rebase and update your plans with the click of a button. Upon accessing an outdated plan in the New Year, you’ll be prompted to rebase your scenario. You click the button, and that’s it — you’re done.

The rebasing will cover all annual updates for income amounts, asset values and costs, RESP grants, debt balances, government benefits, contribution rooms, tax settings, charitable donations, and more. You’ll just want to confirm and validate that all the projected new year values are accurate before proceeding with your plan.

Optimizations

Key elements to compare for opportunities to make improvements.

One of the biggest challenges Advisors bring to us is that they can’t create multiple what-if scenarios for their clients in real time. In Snap, it’s, well … a snap. You can see how quick and easy it is to create multiple what-if scenarios here.

Once you’ve built out multiple what-if scenarios to compare various strategies and potential outcomes, there are some specific areas where you will want to look for tax information and any potential opportunities for improvement.

To compare the scenarios, there are a few areas to review:

- An Estate Summary is available for any year of the plan by clicking the Estate Before Tax value on the Planning page and for the final year of the projection in the report.

- The Marginal and Effective tax rate columns on the Planning page, or on the Cash Flow Summary page of the report.

- The Total Tax paid during the projections, not including estate tax (click the blue icon at the top of the Total Tax column).

- The Estate after Tax column in the Net Worth Projections page of the report for each year for all scenarios.

Clients with corporations

Snap integrates both personal and corporate financial planning seamlessly with an optional corporate planning model (available in our Advisor Business plan) that can be layered onto your personal projections. You can get a brief overview of the module in this video, it’s about 14 minutes long.

You can review the basic corporate assumptions we use here, and learn more about how we handle and track the refundable dividend tax on hand and how to customize your fixed income and equity return allocations here.

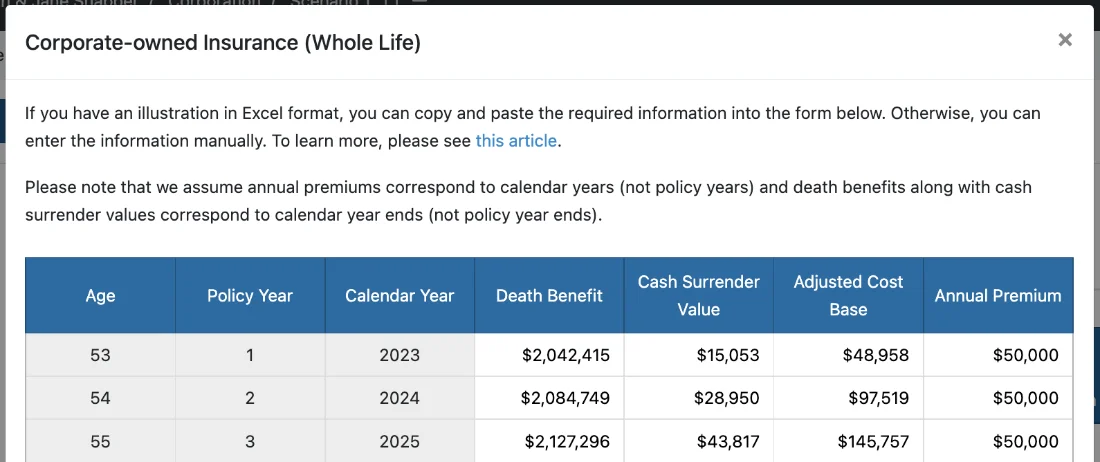

Additionally, there is a dedicated corporate-owned life insurance feature that allows you to enter or paste life insurance quotes of the annual Death Benefit, Cash Surrender Value (CSV), Adjusted Cost Basis (ACB), and Annual Premium.

Snap understands the importance of having those tax planning conversations with your clients. This aspect of financial planning is extremely important to your clients’ overall financial success and health, especially during those retirement and decumulation years. Our goal is to make it as simple as possible for Advisors to model and demonstrate these scenarios effectively in order to help their clients reach their financial goals.

Snap Projections is a leading Canadian financial planning software for Financial Advisors, Planners, and Investment Managers. Snap is transparent, highly flexible, and easy-to-use, specifically created to help small to medium Advisory teams and Independent Financial Advisors serve their clients effectively and efficiently.

Next steps

Snap provides financial planning software for Canadian Financial Planners, Advisors, and Wealth Managers.

Advisors are entitled to a 14-day Free Trial of Snap Projections financial planning software.