Setting a price for your services can seem like a pretty basic aspect of getting started in your own financial advisory practice, but it can also be intimidating. How do you decide what to charge? How will your clients react to your prices?

In the third episode of my five-part interview series with John Page, RFP, CFP, RFC of Wealth Enhancement Academy, and Chairman and Chief Adjudicator of the PlanPlus Global Financial Planning Awards, we’ll be talking about the ins and outs of pricing. Listen to the episode to find out more about how to set your own prices and what mistakes to avoid when doing so.

Topics Discussed in This Episode:

- Different types of pricing models

- Importance of matching your services to the client’s problems

- Why failing to charge for financial planning is a mistake

- The importance of providing a menu of services, and what that menu should look like

- How to establish pricing based on the level of complexity of the client’s assets

- How John Page sets prices

- Why monthly fees are a better choice than annual fees

- What prices a beginning financial advisor should be charging

- The importance of making financial advising simple for clients

Quotes by John:

“Everybody wants to have their problems solved. That’s really the root of it. So your solution is going to solve somebody’s problems.”

“The most common mistake that I see is not charging for the plan.”

“It’s very hard to build the value of the service that you offer unless you’re able to articulate it, unless you have something to show to people.”

Show notes:

– Email John Page at: JPage (at) mywea.net

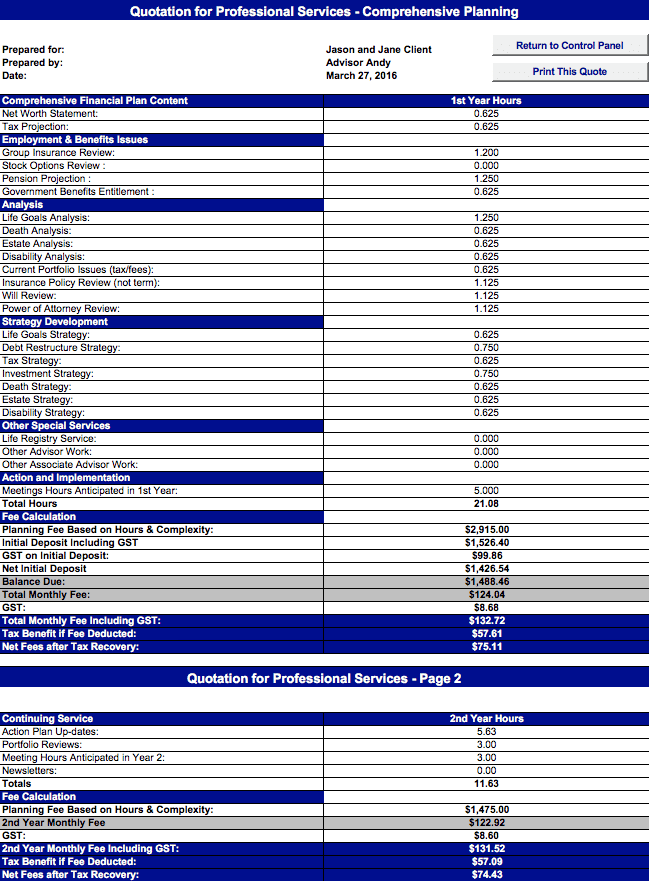

– Quotation for Professional Services – Comprehensive Planning

At the heart of it, you need to have a pricing structure that fits what clients are looking for. As John puts in, “Everybody wants to have their problems solved. That’s really the root of it. So your solution is going to solve somebody’s problems.”

But what exactly does that look like? We’ll start by showing you how to break your service down into parts, and then explain how you can successfully price your service offering to make it irresistible to any prospect.

Why provide a menu of services?

While financial planning menus are not common in the industry, and clients may be surprised to see that you have one, John recommends them because they help to demonstrate the value of what you provide.

According to him, “It’s very hard to build the value of the service that you offer unless you’re able to articulate it, unless you have something to show to people.”

People are familiar with the concept of a menu in other industries and can easily visualize what one looks like. If you can show them exactly what goes into financial planning, they’ll understand the value of the overall work and be willing to pay for that value.

Some planners treat the financial plan as the menu itself. However, John cautions against this.

The problem with that approach is that a financial plan is not just one fixed thing or object. It’s more of a process to solve clients’ financial problems. As John says, “If you think about it, nobody wants a financial plan. What they want is the benefits that a plan can provide to them.”

The benefit is in the process you’re providing to clients to help them achieve their financial goals. Lumping all the possible components of that process into one “plan” simply doesn’t encompass everything you may do for them.

Tip: Break your plan down into component parts to help articulate to clients the potential services you may do for them, and to show them that it’s a process that depends on their exact context and needs.

What should a financial planning menu look like?

A standard financial planning menu may include components that fall into the following sections:

- Initial engagement & conversation

- Investment services

- Investment planning strategy

- Tax planning strategy

- Risk management strategy

- Cash flow management strategy

- Estate planning strategy

- Life management

- Monitoring

Within each section, think about the components that go into that service. For example, under investment services, you might include things like analysing risk tolerance and determining asset allocation.

If you missed it, go back to Episode 1: How to Successfully Transition from Product-centric into an Advice-centric Practice for more on reviewing your own process so that you’re able to articulate it to clients.

To help you out, John is sharing a sample menu of services that can get you started.

Taking on clients with modular needs

Now that you’ve broken down your services, you may be wondering if it’s a good idea to take on clients who want your service for only one aspect of financial planning, like investment advice or insurance.

John’s suggestion is no. He calls these individual services “modular needs” and says that clients may think they only have one such need when really, they would benefit from a whole plan. The reality is that everyone needs some kind of financial plan.

The key is that you can’t possibly extricate one modular need from the rest of a plan. You don’t always have to go in depth into every single area, but you can’t very well help with one part without looking at the overall picture.

Tip: With any financial service or need, there are usually three areas you have to look at, no matter what. They are: disability, death, and retirement.

Existing pricing models

Ok, let’s get down to actually pricing your financial planning service.

Here are just some of the ways financial advisors price their services:

- At the simplest end, some advisors just come up with a single fee for financial planning and charge their clients that fee. This is how John started out.

- Some advisors have a pre-determined pricing structure based on levels ‒ for example, basic, medium, and comprehensive. This actually works fairly well for a number of advisors.

- Most advisors charge only for assets under management and include the financial plan as part of that service.

We want to show you a different pricing model, one that’s based on a very simple formula and actually matches the service you’re providing, every time. It will also prevent you from making the biggest pricing mistake planners can make.

The #1 mistake financial advisors make when pricing their services

John says, “The most common mistake that I see is not charging for planning.” He’s talking about advisors who just charge for assets under management and not for the planning.

Why is this such a big mistake? There are two major reasons:

- It doesn’t fully capture how much work you’re doing ‒ are you really doing ten times more work just because a client has ten times as much wealth as someone else? Probably not.

Think about two clients who each have a million dollars in assets, but one of them has the following:

-

- A couple holding companies

- Assets in a different country

- Multiple insurance policies

You can imagine that any one of these would add a lot of complexity and work for you. Just imagine trying to figure out how all those insurance policies interact with one another! The types of assets matter a lot more than their amount when it comes to the work you’re putting in.

2. Even worse, charging for assets under management and including planning as a kind of free bonus to clients devalues the service. This often happens because advisors don’t see their own work as valuable.

If you’re not charging for your planning work, you’re not presenting it as something that has value. If you don’t show clients that it has value, they won’t see it as valuable, either.

Establishing pricing so that it always fits the service you’re providing

The basic formula John uses to explain costs to clients is this: Time + Complexity.

This formula makes it clear that everyone’s costs might be different depending on their needs. It solves the above example of two clients with the same amount of assets but varied levels of complexity.

Putting a price on time and complexity

So how can you come up with a fair price based on that formula?

John suggests thinking about how long it takes to do each component on the menu. That’s easy to do if you just keep track of how long it takes you to do a specific task.

Think about the following two questions to help you come up with a price range for any individual component:

- How long does it take you to do a particular task?

- What aspects would simplify or complicate that process?

Tip: If you’re just starting out and don’t have a lot of experience yet, look at what someone else is doing to get a good estimate.

John’s practice actually came up with a calculator that you can check out to see how to calculate the cost of an sample client.

Monthly vs annual fees

John suggests that you collect fees on a monthly, rather than an annual, basis. Here’s why:

- For a small financial planning business, the cashflow aspect makes monthly payments invaluable. Recurring monthly revenue is so important.

- A smaller monthly fee is a lot easier for people to swallow than one large cheque. John explains that one planner he was working with charged $1500 per year to do a financial plan. Clients weren’t too keen on going to their annual review and paying a big cheque, so they procrastinated on coming in. Over time, retention became a problem.

- People already have lots of monthly fees, like mortgages, car payments, credit cards, and phone plans. Many of these are even automatic. A monthly fee will feel familiar to clients and can fit into their existing payment schedule.

Tip: Don’t send an invoice every month; instead, have your client sign an agreement so you can make automatic monthly withdrawals. That way the client doesn’t even have to think about it.

Most importantly, a monthly fee also reflects the ongoing nature of financial planning. A client’s financial situation changes constantly, not just once a year, and must be monitored. A monthly fee demonstrates that you’ve got your client’s back all year round, not just when it comes time for their annual portfolio review.

Tip: In addition to a monthly fee, charge a one-time starting fee once they see the initial plan and really understand the value you’re providing. This reflects the large amount of work you’re putting in up front to create a plan that will allow them to achieve their objectives.

John does caution that you need to be clear what a monthly fee does, and does not, mean. Let’s say you’re charging $200 monthly ‒ that doesn’t mean your client should expect you to do $200 worth of services each and every month. Planning work naturally ebbs and flows, with quite a bit of work once or twice a year and a lot less effort for a few months after that. Just because the fee is spread out equally doesn’t mean the work necessarily is, and your client needs to understand that.

So what should you be charging?

John suggests that $80 to $100 monthly is typically a good starting rate. You should certainly never go below $50 per month, and that would be for a very, very simple case.

At the top end? John has found that $1000 monthly is usually the most that a planner will charge.

Whatever you’re charging a client, it’s crucial to highlight the value you’re providing them for that cost. As we discussed in Episode 2: How to Properly Articulate the Value of Financial Advice, showing clients a sample plan and highlighting specific action items to help them meet their goals can work wonders.

Remember, if you don’t value your own services, neither will your clients. If you can understand your own worth and articulate it to clients, they will be willing to pay because they see the value in it.

Making sure your pricing adds value to clients

Let’s say you’re charging a $200 monthly planning fee for an average client and you have 100 clients. Have you just added $240,000 of additional revenue per year?

Well, not exactly.

You can’t just stack planning on top of the asset management you might already be doing. You’ll likely start to charge less to manage assets as part of your financial plan.

Keep in mind that the industry is under a lot of scrutiny and pressure to lower management fees, and commissions have been banned in some jurisdictions. Therefore, charging for planning might be particularly valuable these days.

Especially, if you align your pricing with something else: value.

Your job is to develop a service and process that solves people’s financial problems and helps them meet their goals. Remember that just managing assets doesn’t have nearly as much value as good financial planning.

Tip: Yes, asset management has value, but a well thought-out plan and subsequent monitoring has way more value to your clients, so charge them accordingly.

KEY TAKEAWAY: Keep it simple

All of this might sound a bit complicated the first time you hear it, but remember that at the core, you’re just doing two things:

- Figuring out what people’s problems are, and

- Tangibly solving those problems.

You just need to articulate the value for yourself and your clients (remember those sample plans from Episode 2?) and charge according to that value.

Here are some final words of encouragement from John: “You are a problem solver. You are an objective-getter. You help people reach their financial goals in a very, very tangible way.”

If you want more words of wisdom from John, you can shoot him an email.

With that, get out there and solve people’s problems!

Coming up next, look out for Episode 4: Conducting your First Client Meeting in a Way to Maximize Conversions and to Weed out Bad Clients. We’ll share with you the crucial parts of a great first meeting that will help you get more of the clients you want, and less of the ones you don’t.

If you haven’t already subscribed to the podcast on iTunes, go ahead and do that now to make sure you don’t miss any more expert tips on growing your financial advisor practice. As well, sign up below to get an email notification every time a new episode drops.

{kind=link}

{kind=link}

{kind=link}

{kind=link}