Why client comprehension matters

Interactive charts have become a cornerstone tool for Snap Advisors who want to educate their clients. Have you ever considered how much client comprehension and engagement impacts the financial plan’s chance of success?

Ensuring your clients genuinely understand their financial plans isn’t just beneficial—it’s essential. Here’s why:

Clarity and Comprehension – Financial concepts can be complex, even overwhelming. Presenting information in a clear, digestible way helps clients grasp the details, empowering them to engage confidently in the planning process.

Trust and Confidence – When clients fully understand their financial strategies, they build trust in their Advisor’s expertise. Transparent communication fosters long-term relationships, reinforcing that their best interests are always the priority.

Informed Decision-Making – A well-understood plan allows clients to make more thoughtful financial choices. By clearly outlining risks, benefits, and trade-offs, Advisors help clients align financial goals with their values and priorities.

Implementation and Follow-Through – The more clients understand, the more likely they are to take action. A clearly communicated plan increases commitment, ensuring they follow through with the necessary steps to achieve their financial objectives.

Reduced Stress and Anxiety – Financial uncertainty can be a major source of stress. A well-explained plan provides reassurance, helping clients feel more secure and confident about their financial future. This is one of the many reasons Advisors stress test their clients’ projections.

Stronger Engagement and Collaboration – When clients clearly understand their financial plan, they become more engaged in the process. This fosters meaningful conversations, allowing Advisors to tailor strategies to clients’ evolving goals and circumstances.

Long-Term Success and Adaptability – Financial plans need to evolve with life’s changes. When clients understand their plan’s framework, they can more easily adapt to shifting financial landscapes, making adjustments with confidence rather than hesitation.

At its core, financial planning isn’t just about the numbers—it’s about people. Delivering a plan that clients can truly understand transforms their experience, empowering them to take control of their financial future with confidence.

It starts with presenting the information in a way they can understand.

Watch the video on using interactive charts

Canadian Financial Advisors, Planners, and Investment Managers are eligible to start a 14-day Free Trial of Snap Projections financial planning software.

How can interactive charts transform the way you present financial plans?

Effective communication is key to helping clients understand their financial journey. Snap’s interactive charts offer powerful features that make financial discussions more engaging and insightful:

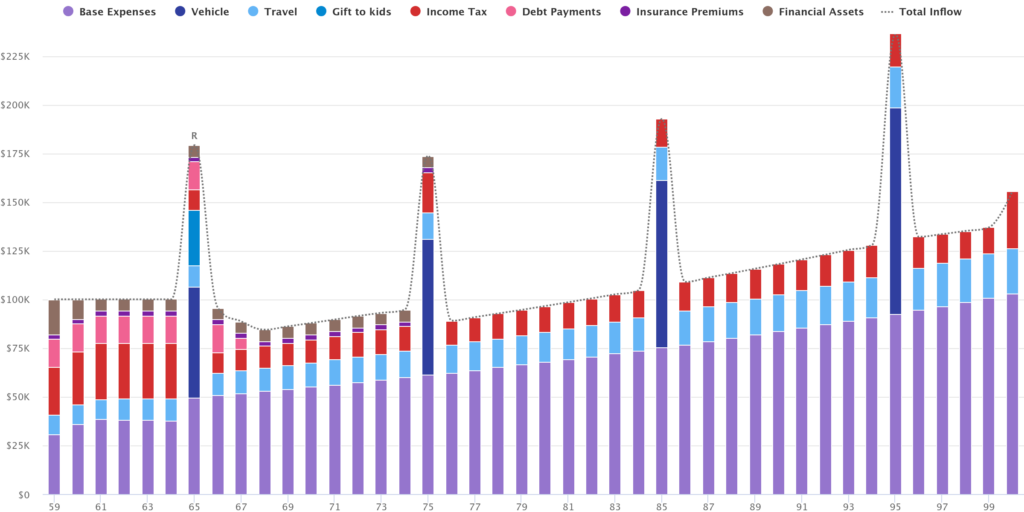

Telling a Financial Story – Visually compelling charts help Advisors present complex information in a way that’s easy to grasp. For example, the Cash Inflows chart illustrates income sources during retirement, providing clients with a clear picture of their financial future.

The Cash Outflows chart categorizes all spending that has been built into the plan, ensuring clients can see everything that matters to them has been accounted for.

The Cash Outflows Chart

Interactive Insights with Mouse-Over Pop-Ups – Hovering over chart elements reveals helpful summaries, making it easy to highlight key milestones or changes over time.

This is particularly useful in the Net Worth chart, where Advisors can draw attention to significant financial events, improving client engagement and understanding.

The Net Worth Chart

Customizable Display for Focused Conversations – Snap’s charts allow Advisors to tailor the view to match the discussion. Clicking on legend items hides or highlights specific data points, allowing for a more focused conversation on particular income sources or assets. Charts can also be displayed in nominal or real dollars for added clarity.

Full-Screen View & Print Options – A full-screen mode increases the impact of visual presentations, while individual chart printing offers flexibility for personalized client take-aways. Whether in a digital meeting or an in-person session, Advisors can adapt their approach to suit each client’s needs.

By leveraging these interactive features, Advisors can transform financial data into a clear, compelling story—empowering clients to make informed decisions with confidence.

Next steps

Canadian Financial Advisors, Planners, and Investment Managers are eligible to start a 14-day Free Trial of Snap Projections financial planning software.

Learn how to leverage interactive charts with a one-page financial plan summary report.