It’s never been easier to provide tremendous value to your corporate financial planning clients. One easy way to improve corporate financial planning advice is through the modelling of life insurance.

Snap now enables the modelling of corporate Whole Life and Universal Life policies within its Corporate module, including the impact on the organization’s CDA balance and the flow of death benefits to the personal side.

Use cases for corporately-owned life insurance

The new corporate-owned life insurance feature in Snap has been designed primarily to address the following two use cases:

- Demonstrate the potential benefit of using excess cash in a corporation to purchase permanent life insurance with the client or spouse as the insured individual for the policy. This strategy can help reduce passive investment income in the corporation, potentially avoiding reductions to the Small Business Deduction (SBD). It may also allow future balances to be distributed from the corporation on a more tax-efficient basis (e.g., through the Capital Dividend Account).

- Demonstrate how corporate-owned life insurance could help provide retirement income. This may be done through borrowing against the Cash Surrender Value (CSV) during the insured individual’s life, or through the use of the Death Benefit to provide income to the surviving partner.

Watch the corporate planning lesson

Why we built this new feature

Why did we develop this new feature for corporate life insurance & how does it benefit your Financial Advisory practice?

Snap users have been asking for this feature for some time now, so it’s been high on our priority list. Building a feature this in-depth was no easy task, and we wanted to ensure we did it right.

Doing it right meant we needed to take the time to conduct extensive user interviews and even change the default logic of the disposition – another added benefit to this product update because you now have even more flexibility and customization options.

Download your free digital marketing guide for Canadian Financial Advisors, Planners, and Investment Managers here.

How Advisors plan to use the new corporate life insurance functionality

Here are some of the new things you can do in Snap’s comprehensive corporate module that’s available in the Advisor Business Plan.

- Show how redundant cash can be extracted from your clients’ corporation(s) more tax efficiently upon the death of a shareholder through the use of corporate insurance policies.

- Easily model how corporate insurance can be used to enhance the estate value of your clients.

- Select either a Share Sale or Wind-up for your corporate disposition on death calculation, with wind-up being the new default.

- Quickly illustrate how corporate insurance can help to support a surviving spouse of a deceased shareholder with income from a corporation – tax efficiently.

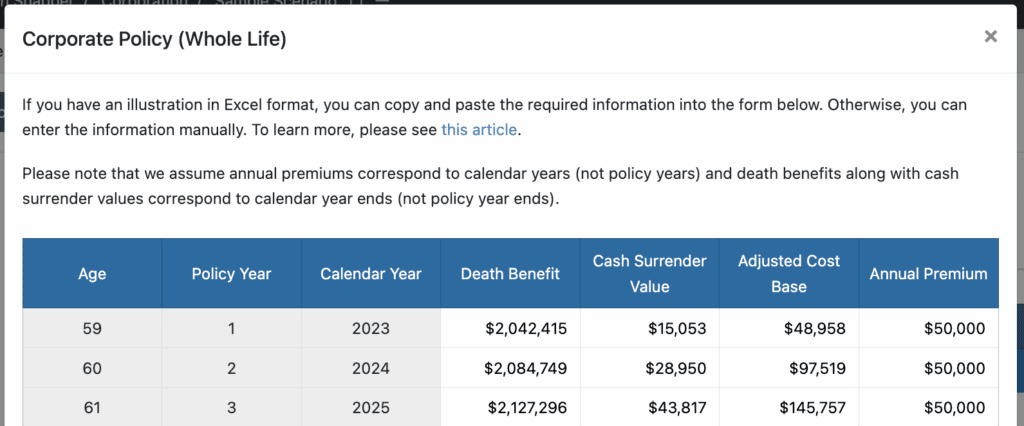

- Conveniently copy and paste policy illustrations from insurance providers right into Snap to expedite the modelling of corporate insurance strategies.

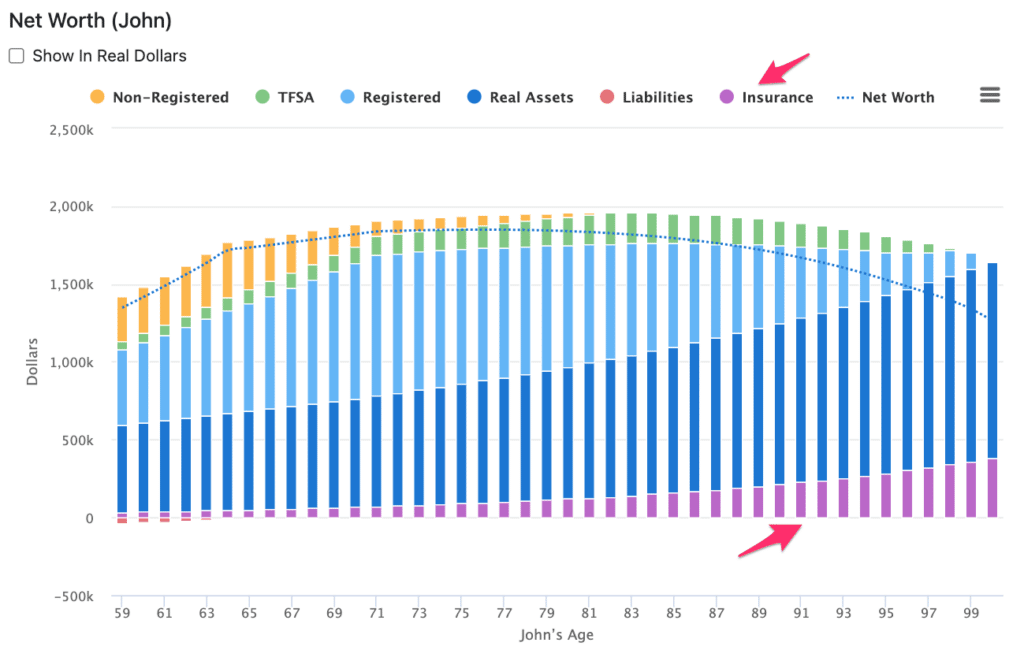

Cash surrender value

You can see the CSV of life insurance policies to the client’s Net Worth. This will be reflected on the Planning Pages, in the Charts, and in the Client Report.

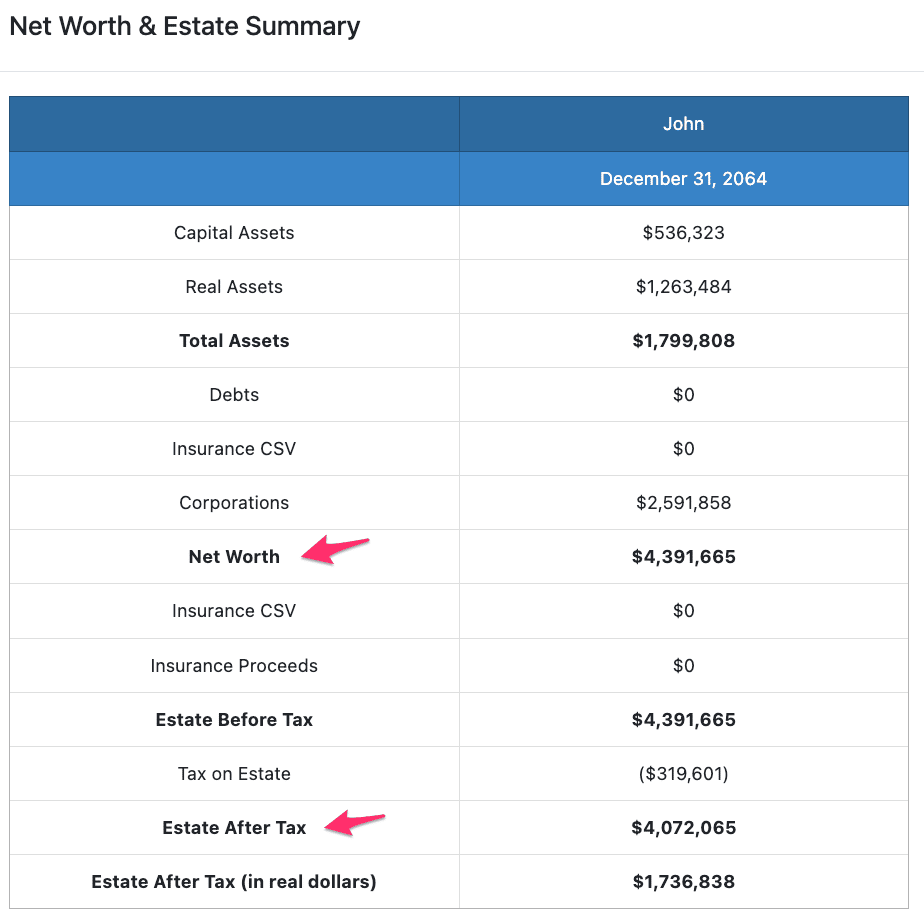

Estate summary

The Estate Summary table’s top section breaks out the Net Worth at year-end (which is what the client can expect to own as of that year). The bottom section breaks out the Estate After Tax that shows how much would be available to the estate if they pass away in that year.

The Snap Projections development team works tirelessly to take the requests of their users and turn them into a reality. Today’s brand new features and updates aren’t a rarity, it’s what you can expect from this passionate and dedicated product team. As your practice grows, the software will continue to grow and evolve right long with you. This is a financial planning platform that was designed for Advisors, with Advisors.